Happy New Tax Year - Six Big Changes To Pay, Tax And Benefit Policy

28th March 2024

The beginning of April brings a new tax year, and a flurry of tax, benefit and pay policy changes coming into effect. Benefit levels are finally returning to their pre-pandemic levels after a difficult few years. Threshold freezes will continue to pull more people into paying tax, but the tax they pay on every extra pound they earn will fall to a record low.

These changes will create a mix of winners and losers, depending on how much you earn, how old you are, and where you live. Higher earning employees gain more from National Insurance cuts than they lose from threshold freezes, while the end of Cost of Living payments will mean lower benefit support for millions of households.

And while over a million renters will benefit from greater housing support, everyone in England and Wales will pay more of Britain's worst-designed tax - Council Tax.

Floor lifting

There is an extra reason to celebrate the new financial year on 1 April - it marks the minimum wage's 25th birthday (you can watch the birthday party discussion here). Low-paid workers have something to celebrate in the here and now - the increase from £10.42 to £11.44 an hour that kicks in on Monday is the third-biggest rise (in both real and cash terms) in the wage floor's 25-year history.

And we should use this quarter-century milestone to take a longer view of its impact. It's been huge. A low earner working full time today earns £6,000 a year more than they would have done had their earnings simply gone up in line with typical wages over the past quarter-century.

The minimum wage also entirely reversed who got the biggest pay rises in Britain. In the 25 years before its introduction, higher earners consistently did best. But since 1999, pay growth for the UK's lowest earners has been five times that of the highest earners.

Our chart makes that a bit more concrete, showing that occupations like bar staff (what I was doing when the minimum wage arrived) and cleaners have seen their wages rise far ahead of the rest of the population (which maybe isn't that hard given the pay stagnation of the last 15 years...). I think it's hard to argue against the idea that this is the single most successful economic policy of my lifetime. If you want more minimum wage charts, read this.

The big benefit catch-up

There are some big benefit increases coming on 8th April, but you should think about them as a catch-up story - recovering the ground lost to massive price and rent rises. As prices have surged in the shops over the past two years, the real value of social security support has dropped significantly as annual uprating has lagged behind the rising cost of living.

Now that inflation is falling back, we are about to reach the point where the rates of most benefits finally return to their pre-pandemic level in real terms, thanks to the 6.7 per cent uprating that will kick in (reflecting last September's CPI figure). This will see the basic rate of out of work Universal Credit rise by £300 a year for a single person, and £900 for a couple with two children.

But it won't feel like catch-up for those on low incomes, because the new financial year will also see the drawing to a close of additional support that government provided in different ways through the pandemic and cost of living crisis.

Specifically, the lump-sum Cost of Living Payments that helped poorer households through the last two years come to an end. Take all these changes together and total annual support in 2024-25 will be £685 lower in real terms than it was last year for a single person, and £110 lower for a couple with two children receiving Universal Credit.

Rent rises

The problem with most benefits has been that they weren't rising as fast as prices in recent years, but when it comes to support with paying rent it was much worse: the cap on support (the Local Housing Allowance) has been frozen at 2019 rent levels for the past four years - four years in which rents have surged (keep an eye out for forthcoming Resolution research on why that has been and what comes next). This has led to large and geographically uneven hits to low-income privately renting households, and contributed to record homelessness.

The Government has recognised this is unsustainable and the very good news for around 1.3 million private-renting households currently capped by the LHA is that it will be repegged to local market rent levels in April. This will mean a large catch-up in areas where rents have risen the most in the last four years: maximum support for a three-bed property will rise by £81 per week in Bristol, £62 in South East London, and £51 per week in Glasgow, for example.

This is good news, but there are caveats. First, thousands more families will now run into the benefit cap (which hasn’t been lifted to reflect the LHA change) so won’t see the full impact of this change. A couple with two children on Universal Credit and paying rent at or above the Local Housing Allowance will now be benefit capped in four-in-five (83 per cent) local areas, up from just over half (53 per cent) in 2023-24. Oh, and the Government is trying to pretend it can now go back to freezing the LHA in future years, allowing exactly the same pressures that have just proved unsustainable to build again as rents rise.

Reducing rates

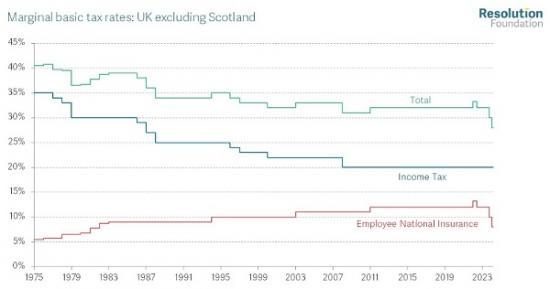

Did you enjoy the 2p National Insurance (NI) cut in January? Well you get the same again next week (if you’re below the state pension age...). The self-employed among you will get your full 3p cut (and no longer need to pay the flat rate Class 2 NI charge). Leaving aside whether we can afford these £20 billion-a-year tax cuts (we probably can’t), this is a big change, taking the main employee NI rate to its lowest since the early 1980s. The combined basic Income Tax and employee NI rates haven’t been this low since at least 1975. This drift down in headline tax rates is one of the big tax stories of the last four decades.

Talking of reducing marginal tax rates, next week will also see the threshold at which Child Benefit starts to get tapered away rise to £60,000. Plus, the rate at which it is tapered away will halve. This will ensure no basic-rate payers will lose any Child Benefit, and remove some of the more bonkers marginal tax rates that people can face. Almost half a million families will gain an average of £1,260 each.

Frozen thresholds

While marginal tax rates are falling, taxpayers are losing out through frozen tax thresholds - many of which would ordinarily have risen by 6.7 per cent this April. After years of these freezes during a high inflation phase, the real value of the personal allowance (how much you can earn before paying income tax) is down a lot. By 2027-28, it looks like around 60 per cent of the 2010s’ allowance increases (the signature tax policy under David Cameron and George Osborne) will have been reversed (pensioners meanwhile have had the recent tax rises but didn’t win from those previous tax cuts because age-related tax allowances were abolished).

Amusingly (as tax facts go), the personal allowance rollercoaster is likely to leave its level just where it would have been if the earlier default policy of raising the allowance in line with RPI inflation had simply continued. Always nice to get back where you started.

Council Tax crescendo

Income taxes are up for some and down for others next year. But there’s a much simpler story for Council Tax: it’s going up a lot for almost everyone in England and Wales (with average increases of 5.1 per cent and 7.7 per cent respectively). This is part of a longer-term trend of national government making decisions that mean we’re more reliant on Council Tax to raise revenues (most recently by creating a situation in which councils are going bust). The revenue from Council Tax and its predecessors has been rising as a share of GDP since its low in the early 1990s (after the poll tax debacle). The Council Tax take will reach a record high (leaving aside the Covid-19 period when GDP plummeted rather than Council Tax rising) of 1.7 per cent of GDP in 2024-25.

Never-ending above-inflation rises are then expected, so this is projected to keep rising to 1.8 per cent in the next parliament. The problem? We’re becoming more reliant on a tax that is chronically unfair (e.g. lowest in the richest parts of the country) and way out of date - Council Tax is still based on valuations from 33 years ago.

You win some, lose some

Unsurprisingly, with so many changes happening at once, the new fiscal year will affect lots of you in very different ways. There’s very good news for some: a higher earning parent on £60,000 may get a net £900 tax cut, plus a reinstatement of Child Benefit (at least £1,300), potentially plus 15 hours a week of free childcare (which is being increased).

And a 21-year-old on the minimum wage may get a £2,500 (gross) pay rise. But the end of Cost of Living Payments will be a particular blow for some; and a basic-rate taxpaying pensioner will essentially see their above-inflation State Pension rise (£190) wiped by this April’s personal allowance freeze (£170).

Inevitably, then, some may be more likely to be celebrating next week than others but, whichever you are, hopefully this round-up helps you keep on top of what’s going on.

Read this report with graphs at Resolution Foundation