An Inherited Problem - Inheritance Tax Affects The Most Wealthy

8th June 2024

There has been recent speculation that the Conservative Party might announce that they intend to abolish - or significantly reduce - Inheritance Tax (IHT) if re-elected. Calls for cutting or abolishing IHT are frequent, given the tax's unpopularity - despite the fact that only a small minority of people will ever be likely to pay it. In this Spotlight, we put such a policy in context by setting out some of the key facts about IHT.

Overall, IHT receipts amount to less than 1 per cent of total tax revenue, at around £7 billion, with only 3.7 per cent of UK deaths resulting in an IHT charge. But this is expected to grow in the coming years not least because payment thresholds are frozen until April 2028. The current IHT system does have its flaws - most obviously, a large number of associated reliefs mean that IHT is easy to avoid for the wealthy and well-advised. These issues suggest that the ideal approach would be to reform, rather than abolish, IHT. A well-functioning IHT could play a key role in mitigating the risk of inheritances increasing wealth inequality.

Only a small minority of estates are subject to IHT, but its salience is likely to rise

As things stand, only 3.7 per cent of UK deaths (or 27,000 estates) resulted in an IHT charge in 2020-21. In fact, the proportion of UK deaths that have resulted in an IHT charge has been broadly flat since 2016-17. This is likely thanks to the introduction of the Residence Nil-Rate Band (RNRB) in 2017-18 offsetting the impact of rising asset prices.

Given the small number of estates that are subject to IHT, overall receipts are a very small proportion of overall revenues. IHT receipts totalled £7.1 billion in 2022-23, less than 1 per cent of total tax revenue. This compares with an estimated flow of inheritances and gifts of around £150 billion a year pre-pandemic, an effective tax rate of just 4.7 per cent.

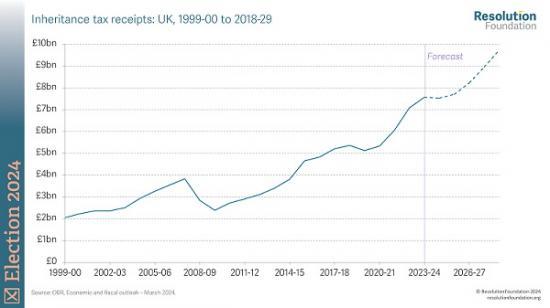

As shown in Figure 2, IHT receipts have been growing steadily and this is forecast to continue. In 2028-29, IHT receipts are projected to rise to £9.7 billion, though this would still be less than 1 per cent of total tax revenue. This rise reflects the fact that IHT thresholds have been frozen until April 2028, meaning that the proportion of estates triggering a tax bill is projected to rise to over 6 per cent by 2028-29, or 44,000 deaths.

IHT's salience is likely to rise further still as the estimated value of intergenerational transfers (both gifts and inheritances) is set to double over the next two decades as the large baby-boomer cohort start to bequeath their wealth (Figure 3). Scrapping inheritance tax would, therefore, come with a growing fiscal cost.

Various reliefs make it possible for IHT to be avoided by the wealthy and well advised

Different inheritances can be taxed in a variety of ways causing inequity within IHT. A key cause of this unfairness is the presence of Business Relief and Agricultural Relief, which can potentially exempt a wide range of assets from IHT. In 2022-23, HM Revenue and Customs estimate that Business Relief cost an estimated £1.3 billion and Agricultural Relief cost £365 million. Previous work has shown that these reliefs are very concentrated among a small number of estates. Indeed, as shown in Figure 4, in 2019-20, only around 1,170 estates claimed Agricultural Relief and 2,820 claimed Business Relief, with 53 per cent of Business Relief going to 113 estates (the top 4 per cent). These reliefs contribute to the fact that the wealthiest estates pay a lower effective rate of IHT than less-wealthy ones.

Another major Inheritance Tax break is the residence nil rate bank (RNRB). The introduction and growing generosity of the RNRB increased the total IHT-free threshold from £650,000 for couples in 2016-17 to £1 million today. As a result, it remains quite possible for someone to inherit tax-free almost four averagely priced homes. The extra allowance only applies to main residences and only when these are passed on to direct descendants. Nevertheless, it is a large tax relief, significantly reducing how many estates pay any IHT and costing £1.8 billion in 2023-24.

IHT isn't perfect, but there are economic and social reasons for having such a tax

Despite only a tiny minority of people paying IHT, it is perceived poorly by the public in general. In recent survey evidence, a majority of people (55 per cent) say that inheritances should always be tax free; only 29 per cent thought the current system was the right one.

Despite its unpopularity, there are economic and social reasons for having a well-designed IHT. Wealth gaps in the UK are large, and with increases in wealth outpacing those in incomes, wealth has become more important in driving life outcomes. In this context, Figure 5 shows that that scrapping IHT risks entrenching high wealth, as higher-income people are more likely to have received an inheritance. For instance, across the population aged 20 and above, a person in the top fifth of the income distribution was four times more likely to have received an inheritance than someone in the bottom fifth of the income distribution. A well-functioning IHT, therefore, has a role to play in limiting the impact that wealth transfers have in increasing inequality.

Moreover, measures that lead to lower IHT revenues would add to the problems of our current stretched public finances. In recent work we have shown that, if the uncertainties surrounding the fiscal outlook turn into bad news after the election, this would create a £12 billion shortfall relative to both parties' commitment to get debt falling by the fifth year of the OBR forecast (and if the next government want to avoid a return to austerity that gap would rise to around £33 billion).

Overall, the problems with the IHT suggest that an ideal approach would be to reform rather than abolish the tax, with reforms focussed on tightening reliefs.

Read the full report HERE

Pdf 5 Pages

Our Social Media