Does Raising Public Sector Pay Above Inflation Risk Further Inflation?

24th August 2024

The Labour Government's decision to raise the salaries of train drivers triggered a heated debate. Some argue that the pay rises will lead to inflationary pressures. Others believe this concern is overblown. Costas Milas goes over the data and finds that pay rises are likely to unleash some inflationary pressures. He advises the Bank of England to resist lowering interest rates at the pace expected by financial markets.

In a highly critical editorial of the new government's policies, The Times noted that Labour's "capitulation" to the earnings demands of train drivers opens the door for inflationary pressures. The risk is that additional strikes by other workers who (perhaps rightly) also feel underpaid becomes a "green light" for more inflationary pressures. Larry Elliott, economics editor of The Guardian, disagrees. He argues that the risk of a wage-price spiral is overblown and that there is public sympathy for unions seeking to protect the living standards of their members following the recent surge in inflation.

All these developments follow the decision by Chancellor of the Exchequer Rachel Reeves to authorise above-inflation public sector pay rises of 5.5 per cent. The announced pay rises comfortably outpace the Consumer Price Index (CPI) inflation rate. The CPI rose slightly to 2.2 per cent in July, from 2 per cent in May and June.

The idea of the latest public sector settlements is that public sector workers will restore some of their purchasing power, after it took a "hit" because of recently high inflation. Presumably, Reeves also has faith in the efficiency earnings hypothesis, which states that higher earnings will make (public sector) workers more productive. Bank of England (BoE) Governor Andrew Bailey expects these pay settlements to have a "very small" impact on inflation, without, so far, providing any detailed evidence regarding his assessment. The pressure on BoE's policymakers is definitely on, not least because brand-new academic research of mine (co-authored) finds that the quality of institutions rather than inflation targeting by Central Banks (including the BoE) delivers low and stable inflation.

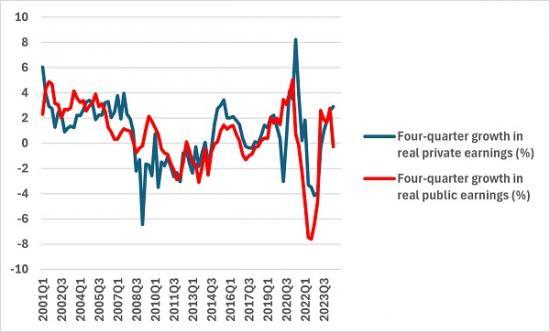

The key question is: do above-inflation public pay increases risk triggering a wage-price spiral? The Office for National Statistics (ONS) database provides data on average weekly private and public sectors' total earnings since 2000.

Figure 1 plots the four-quarter growth in real private sector earnings (nominal growth minus CPI inflation) together with the four-quarter growth in real public sector earnings. Real private earnings have grown by an average of 0.78% per annum, slightly higher than the average growth rate of 0.61% per annum in the case of real public earnings. The drop in real public earnings growth in 2024Q2 has been skewed by the fact that large one-off bonuses were paid to NHS staff in 2023Q2.

I am interested in assessing the possible inflationary impact of (the announced) increases in public earnings. To do so, I rely on an econometric vector autoregressive (VAR) model which looks at the dynamic interrelationships of four variables: (a) four-quarter growth in real private earnings, (b) four-quarter growth in real public earnings, (c) four-quarter productivity (output per hour worked) growth in the UK economy, and (d) price surprises or accelerating inflation, the latter proxied by the four-quarter difference in the UK CPI inflation rate. I estimate the model over the 2001Q1-2024Q2 period. The idea is to assess whether a positive growth in real public earnings triggers accelerating inflationary pressures once I control for movements in real private earnings and productivity gains.

Figure 2 below estimates the statistical response of price surprises (or accelerating inflation) together with the corresponding 95 per cent confidence intervals (based on 5,000 bootstrap replications) to different economic shocks over a period of 10 quarters. I note the following:

A positive shock to real public earnings growth does not lead directly to accelerating inflation as the estimated effect is statistically insignificant. This is reassuring and confirms Andrew Bailey‘s recent assessment.

Nevertheless, a positive shock to real public earnings growth lifts real private earnings growth for up to five quarters, the latter also triggering an acceleration in CPI inflation. The acceleration in CPI inflation is not instant, however, as it occurs from quarter four onwards in the order of 0.4 percentage points and for a total of four quarters. Therefore, higher growth in real public earnings affects inflation indirectly through its impact on real private earnings. The impact on inflation is not felt immediately. Instead, it takes up to four quarters to show up in inflation data. I also note international evidence for 18 OECD countries (including the UK) that approximately 50 per cent of the growth in real public earnings is passed on to real private earnings. Not everybody agrees. A May 2022 Bank of International Settlements report argues that the risk of public earnings rises spilling over to the rest of UK earnings is low. Notice, however, that this very report has not considered the big inflation movements during most of 2022 and in 2023-2024.

A positive shock to real private earnings growth does not affect the growth in real public earnings.

A positive shock to the growth of real public earnings does translate into higher productivity growth for up to three quarters, therefore giving some validity to the efficiency earnings hypothesis! In other words, pay, for instance, teachers and NHS staff above-inflation wages to boost their morale and, at least temporarily, their productivity!

What about the impact of labour disputes on pay settlements and, therefore, inflation? ONS data on labour disputes (that is, working days lost due to strike action) become handy. A wage bargaining shock leads to the conclusion, from Figure 3, that a positive shock to labour disputes leads to higher real private earnings some four quarters later (and for a total of four quarters). But also to higher real public earnings some three quarters later (and, again, for a total of four quarters). As I am writing this piece, it looks like a new wave of UK strikes might be on the way as pay deals spur unions to bargain harder. Such strikes will lift wages across the economy and add to (significant) inflationary pressures.

On the policy front, the results here suggest that the latest public sector pay rises will trigger inflationary pressures from around the second half of 2025 onwards. The BoE's latest Monetary Policy Report predicts modal CPI inflation (that is, the most likely CPI inflation outcome) of 2.4 per cent in the third quarter of 2025 based on (market expectations of) an easing of the bank rate to 4.2 per cent and without any consideration of possible inflationary risks emerging from the latest public pay settlements. My results suggest it might be prudent to resist the pace of monetary easing financial markets currently expect.

Author

Costas Milas

Note

This article is from the LSE Blog. To read it with links and more graphs go HERE

This blog post represents the views of the author(s), not the position of LSE Business Review or the London School of Economics and Political Science.