The Problem With Rachel Reeves Plan To Boost Britain's Pension Pots

26th August 2024

Britain has a pension problem. Despite having one of the biggest and most sophisticated financial centres of the world in London, the country's pension industry does not fall into the same category.

The results can be seen in how its funds perform. In 2022, the return on the investments of UK pension funds was -25.4% in real terms, that is after adjusting for inflation. The comparable figure for Australia was -7.6%, and for Canada -8.9%.

This is part of the reason why Chancellor Rachel Reeves has announced she wants UK pension funds to copy their counterparts in Canada and make more money through large investments.

It sounds like a good plan, but there may be some significant problems with it. The UK pension industry, unlike the Canadian one, is dispersed into many small funds, and burdened with poor governance. It lacks transparency, monitoring and appropriate regulatory oversight.

Even if the regulation was changed overnight, and pension funds magically reduced their current investments to release cash to invest in private equity, the UK pension industry is unlikely to become a twin sister of the Canadian one.

The Canadian pension funds are big and run by highly skilled and independent boards. The Canada Pension Plan (CPP), which is the seventh largest pension fund in the world, can serve as an example.

In March 2024 it had about US$420 billion (£322 billion) assets under management. It is formally state-owned, but it is not run by the state but by the independent, professional CPP Investment Board that is accountable to parliament and reports through the minister of finance.

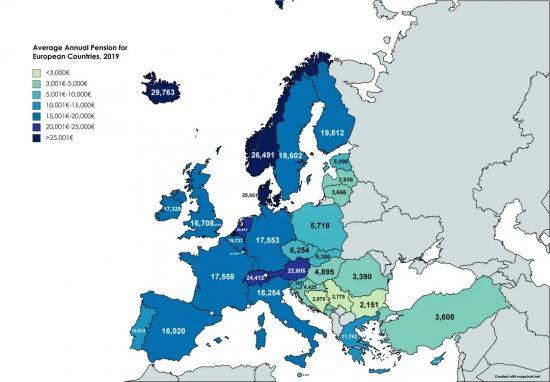

It was only in 2021 that the American financial services firm Mercer upgraded the UK pension industry from C+ (a system that has major risks and shortcomings that should be addressed) to B (a system that has some areas for improvement). This is still far below the grade A given to the pension systems in the Netherlands, Denmark, Iceland and Israel, and B+ in Australia, Finland and Singapore.

Various steps have been taken to fix issues over the last three decades, but these reforms were more "hole patching" exercises than attempts to solve the deeper problems. They focused more on improving coverage (for example by increasing the number of people saving for retirement) than addressing the issue of poor fund performance and high charges.

There have been many years of experimenting with various adjustments to the UK pension industry, including replacing occupational defined benefit (DB) schemes with (often private) defined contribution (DC) schemes. In DB schemes retirement income is linked to individual salaries, whereas in DC schemes retirement income depends on how pension funds perform.

Superhero pension systems the UK could copy

In 2021, Boris Johnson and Rishi Sunak, who were at the time prime minister and chancellor respectively, crafted a letter postulating an "investment big bang", and listing Canada and Australia as the examples that the UK should learn from.

The lesson to be learned was to invest in UK assets the way overseas investors do. Johnson and Sunak lamented that only "UK institutional investors are under-represented in owning UK assets".

But despite what these politicians said, if the UK funds were to learn one thing from the Canadian and Australian superheroes, surely it would be that they should make the best from international investments and not flood the domestic market only because politicians say so.

After Sunak, the next chancellor, Jeremy Hunt, narrowed his desire to transform the UK pension industry to become more like the Australian one..

Now, Reeves is encouraging UK pension funds to invest in infrastructure projects, as they do in Canada, to help spark her plans for growth in the economy.

"I want British schemes to learn lessons from the Canadian model and fire up the UK economy, which would deliver better returns for savers and unlock billions of pounds of investment," she said.

UK trustees lack investment skills

Strong governance, professionalism and accountability of the Canadian pension fund's boards are the pillar of the system. In contrast, UK pension funds are overseen by trustees who often lack the required investment skills, and hence can only provide a limited level of oversight and monitoring.

According to the Pension Regulator's survey, in 2019, only 6% of 447 surveyed trust-based occupational DC pension schemes satisfied all five key governance requirements (KGRs). As many as 62% did not meet any of the KGRs that applied to them.

The governance in schemes that do not benefit from employers' direct oversight (such as group pension or personal pension schemes) face even greater governance difficulties. The costs of such poor governance are high, drag the whole industry down, and are paid directly by pension contributors.

My own research shows that the introduction of independent governance committees (IGCs) by the Financial Conduct Authority in 2015, had a significant impact on the quality of governance of the group personal pension plans.

Even if these committees were far from perfect and were criticised for their lack of independence (only 25% of the surveyed investors were positive about the governance oversight provided by IGCs), their impact on fund performance was noticeable especially for smaller funds, in other words, those that are more likely to suffer from poor governance and skills.

There is no doubt that a continuation with the low-risk investments policy (especially if concentrated on investing in government bonds) is unlikely to deliver sufficient retirement pots or serve the economy well.

However, if the British pension savers are to benefit from the change, the chancellor, or any policy maker and regulator thinking about improving the UK pension system, should start by fixing the shortcomings of governance, rather than pushing inexperienced trustees into the deep waters of private equity investing.

Author

Ania Zalewska

Research Chair and Professor of Finance, Leicester University School of Business, University of Leicester

Note

This article is from The Conversation web site To read it with links to more information go HERE

Our Social Media