Sterling Hits All-time Low: Two Things Can Turn This Around But Neither Is Straightforward

27th September 2022

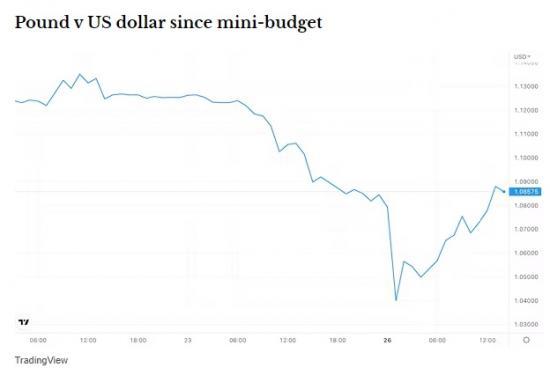

While most people in the UK were still in bed in the early hours of Monday morning, the pound dived. It fell over 4% during Asia trading to reach its lowest ever level against the dollar of US$1.035, while also hitting €1.079 against the euro. This was an exceptional fall, and continues its 3% decline against the US dollar on Friday in response to the hefty borrowing and tax-cutting in Chancellor Kwasi Kwarteng's mini-budget.

In parallel, traders have been dumping British government bonds, which is driving up long-term interest rates or yields. The yield on ten-year bonds, which heavily influences mortgage rates and other bank lending, is now above 4% for the first time since its highs following the 2007-09 financial crisis.

The pound rebounded back above US$1.08 in the hours after the European markets opened, while ten-year bond yields have also eased a little. It is possible that the pound crash during the Asia session was over-extended because trading volumes in the British currency are lower, which makes it easier for smaller amounts of money to make a bigger impact on the market. It is not uncommon for lows to be made in early Asia trading, as has been the case in previous currency crashes.

On the other hand, many analysts think the pound reaching parity with the US dollar is increasingly likely. So where is all this heading and what will the consequences be?

The mini-budget gamble

The pound has already been weakening for over a year. This is partly because the US dollar has been getting stronger as the US Federal Reserve has raised interest rates and reduced the supply of dollars to try and get inflation under control, and partly because the UK with its exposure to high gas prices and post-Brexit challenges does not look like a great prospect for economic growth.

The new Truss government's economic and fiscal policies have made the market even more uneasy. They are based on a combination of energy subsidies and huge tax giveaways - particularly to high-income households and homeowners - which will increase annual borrowing by more than £100 billion.

The tax-cutting, which covers £45 billion of that increase, is a shift away from the direct transfers of money from governments to households and businesses that have been used to help maintain consumption since 2008 in the UK and many other countries. The benefits of tax-cutting in stimulating the economy are more delayed, which makes them more uncertain than direct handouts. In a situation where there is arguably a need for immediate action to support consumption because people's purchasing power is being eroded by rising inflation, direct cash transfers would have been faster acting.

Tax cuts may not even work here. People in the UK may well see the negative reaction from the markets and become more pessimistic about the prospects for the economy. If so, they are likely to spend less, which would weaken growth as opposed to increasing it in the way that the government is hoping for. The government deficit - the gap between how much it spends compared to how much it brings in - would then increase and the tax cuts would be counterproductive.

Either way, the weaker pound is going to further exacerbate UK inflation by making imports more expensive. At the same time, the rise in bond yields will potentially damage growth by increasing lending costs and making consumers feel poorer. It will also make the extra government borrowing in the mini-budget even more expensive than it was going to be already. All of this is likely to put further pressure on the public finances.

This is all a reminder that politically motivated economic policy does not sit well with the markets. With the government stimulating while the Bank of England is tightening monetary policy by raising rates, they are also acting as two opposing forces when it would be better for them to coordinate with one another.

What a turnaround looks like

It is nevertheless possible that the pound is now steadying amid speculation that the Bank of England may intervene with a rate rise to support the currency. This would echo the Japanese central bank's recent intervention to support the yen, which is also in a historic decline against the US dollar.

Yet if the Bank of England does raise headline rates, possibly by 0.5 percentage points or more, this would have a detrimental effect on business financing and economic activity by further increasing the likelihood of higher rates on mortgages and business loans. This might completely negate the government's attempts to support the economy by cutting stamp duty and reversing the planned corporation tax hike - again undermining the growth plan.

The bigger question is what happens to US inflation. If it were to fall thanks to a drop in the cost of energy imports and an improved global supply chain, the Federal Reserve may pivot on monetary policy. This would entail a pause on recent interest-rate increases or even the start of a reversal, which would take pressure off currencies such as the pound and help rescue the UK economy.

Only then would the supply-side measures in the mini-budget geared towards helping businesses with lower corporation tax, simpler planning and low-tax investment zones bear fruit. Even then, the government would have to hope that consumer and business sentiment had not deteriorated too much in the meantime. That all amounts to an extraordinarily risky gamble - if it doesn't pay off, expect more trouble ahead.

Note

This article is from The Conversation web site To read it with more graphs and links to more information go HERE