Election 2024 - Polling Shows Voters Don't Believe The Tax Pledges - Here's How The Numbers Stack Up

5th June 2024

The two main parties contesting the UK general election have been unusually cautious on their spending plans, despite urgent calls for more public funding to tackle crises in housing, social care and the environment.

While they have pledged not to raise income tax, national insurance or VAT, they have refrained from promising tax cuts, despite evidence of these helping to sway past elections.

But recent polling suggests most voters just don't believe any future government can stay within the current fiscal rules without raising tax rates.

The Conservative and Labour parties have pledged to follow the same rules, under which the government's underlying debt must be falling (as a percentage of GDP), with a budget deficit below 3% of GDP, within five years.

The most recent budget stays within these rules - just. But it relies on official projections showing public-sector net debt dropping to 94.3% of GDP in 2028/29, from a peak of 98.8% in 2024/25.

That forecast rests on some optimistic assumptions, especially on the revival of private-sector productivity growth and efficiency savings in public services.

And this is only achieved by committing future governments to significant, unspecified spending cuts beyond the present tax year.

Taxes have already risen

The main parties have pledged not to raise the main rates of income tax, national insurance contributions or VAT, which together account for almost 60% of all tax revenue.

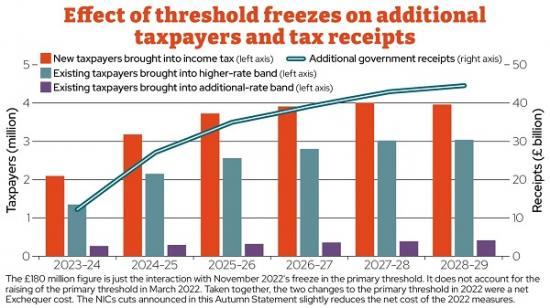

That's not as generous as it seems, as the country has recently experienced a concealed tax increase. Because income tax thresholds haven't risen in line with inflation, many thousands have started to be taxed or moved to a higher tax bracket, the process known as "fiscal drag".

Helped by this, the share of national income paid in taxes is now above 35.5% of GDP and is forecast to reach 37.7% by 2028/29, the highest rate since the second world war.

But inflation is a double-edged sword, because it has also raised the cost of providing public services. And because over-target inflation caused interest rates to rise, the government is paying significantly more for its borrowing.

On top of the self-imposed fiscal rules, the main parties are agreed that certain areas of public spending - notably the NHS, schools, childcare and defence - should rise at least as fast as inflation. They are also committed to the "triple lock" that keeps the state pension growing at an annual 2.5%, even if inflation and wage growth fall below this.

Spending cuts must therefore be focused on other areas. So in real terms the budgets for policing, local government support, social care and other "unprotected" areas have been falling for many years, and must again bear the brunt of the cuts the chancellor has pencilled in.

While insisting that they can make their money go further by cutting waste, successive governments have tackled costs by holding down public-sector pay. This fell on average by 0.3% in 2019-23 and is still 1% lower than in 2007 in real terms, whereas average private-sector pay rose by 2.3% in 2019-23 and 4% in 2007-23.

Those falls provoked strikes across the health, education and transport sectors in 2022 and 2023. But a bigger problem has been public employees voting with their feet, leading to worsening labour shortages. These can only be remedied with significantly larger pay rises, further limiting the extra output that future public spending increases will actually buy.

Public investment has been another easy target for past spending cuts, and is now down to around 1.5% of GDP, one third of its 1945 level when the incoming government faced similar reconstruction tasks.

But cutting the public capital budget could prove to be a false economy, since it has slowed the environmental, industrial and infrastructure projects that contribute to GDP growth in the longer term. Economists have highlighted the constraint on public investment under current fiscal rules as a key reason that they might need to change.

Politicians on all sides still insist that they can spend more, while keeping the main tax rates unchanged and without breaking the fiscal rules. The best way to ease the constraint is still to kickstart GDP growth, which has shown no great resurgence since the COVID pandemic.

But to grow the economy faster, the next government will have to tackle stagnant productivity and labour shortages in key areas that have worsened since Brexit. Liz Truss's 2022 "mini-budget" failed to persuade financial markets that tax cuts and higher spending would pay for themselves by solving the productivity puzzle. That cast a long shadow over any future "dash for growth".

Raising productivity is especially difficult in the public sector, because it focuses on labour-intensive services where output is hard to raise without massive additional recruitment or sacrifice of quality.

Artificial intelligence may eventually allow medical, educational, judicial and other public services to be delivered by machine, or less-trained staff. But this technology-driven public-sector productivity boost, if it happens at all, won't come fast enough to free the next government from unpalatable choices.

No politician wants to admit that tax rises may be needed, when the tax burden is already at its highest since peacetime records began. The all-round caginess on tax and spending intentions is an admission of how tightly the present chancellor has tied the hands of the next.

Politicians on all sides still insist that they can spend more, while keeping the main tax rates unchanged and without breaking the fiscal rules. The best way to ease the constraint is still to kickstart GDP growth, which has shown no great resurgence since the COVID pandemic.

But to grow the economy faster, the next government will have to tackle stagnant productivity and labour shortages in key areas that have worsened since Brexit. Liz Truss's 2022 "mini-budget" failed to persuade financial markets that tax cuts and higher spending would pay for themselves by solving the productivity puzzle. That cast a long shadow over any future "dash for growth".

Raising productivity is especially difficult in the public sector, because it focuses on labour-intensive services where output is hard to raise without massive additional recruitment or sacrifice of quality.

Artificial intelligence may eventually allow medical, educational, judicial and other public services to be delivered by machine, or less-trained staff. But this technology-driven public-sector productivity boost, if it happens at all, won't come fast enough to free the next government from unpalatable choices.

No politician wants to admit that tax rises may be needed, when the tax burden is already at its highest since peacetime records began. The all-round caginess on tax and spending intentions is an admission of how tightly the present chancellor has tied the hands of the next.

Author

Alan Shipman

Senior Lecturer in Economics, The Open University

Note

This article is from The Conversation web site. To read it with links to more information go HERE