Oil and Gas - Are There Thousands Of Jobs At Risk In The North East Of Scotland?

23rd June 2024

Oil and Gas has come up in many of the election broadcasts in Scotland so lets take a look at an article by Mairi Spowage the Director of the Fraser of Allander Institute published on 5 June 2024.

As we enter the third week of the election campaign, the policy announcements from the main parties are coming thick and fast.

One issue that has come up a number of times in the last week (including the party leaders' debate on Monday night) has been the future of the oil and gas industry in the North Sea, and the jobs that are linked to that. Aberdeen and Grampian Chambers of Commerce (AGCC) put out a report last week that said that the new UK Government had "100 days to save 100,000 jobs in the North Sea" which investment analysts said could be lost by Labour proposals to reduce investment allowances linked to the Energy Profits Levy. AGCC reported that this represented a loss of half of the direct and indirect jobs supported by offshore activity.

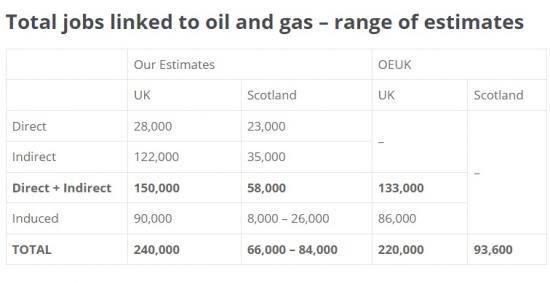

The claim above suggests that activity in the North Sea, directly and indirectly, supports roughly 200,000 jobs. This is a figure that is likely to have come from the Offshore Energies UK (OEUK) Economic Report, which is published annually by the sector body. Their most recent report estimates that domestic oil and gas activity supports 220,000 jobs in the UK.

We've looked at official data and crunched the numbers below - and come up with numbers that are very similar. The important point to note is that this is a number for the UK, not for Scotland. You can see our workings below including our calculations specifically for Scotland - or skip to the end to see the "more important point".

The OEUK numbers

The OEUK report estimates that 93,600, or 43%, of the 220,000 jobs are in Scotland.

It is also important to understand what "support" means. When presenting jobs figures like these, there are three key types of jobs supported:

Direct - jobs in the oil & gas sector itself (where the "oil & gas sector" can vary in scope depending on industries included or excluded)

Indirect - supply chain jobs that are supported by the purchases of the oil & gas sector

Induced - The direct and indirect jobs pay wages which are spent on household goods and services, further supporting jobs (e.g. in cafes, shops etc).

These definitions are standard practice in demand-side economic modelling. The direct, indirect and induced job numbers all relate to GROSS impacts of oil and gas. That is, if Scotland never had an oil and gas industry then many of its current employees would likely have worked in other industries. Perhaps some would not be in employment and others would earn lower salaries.

The induced figures explore the wage spending impacts of jobs supported directly and indirectly and so are less likely to be an entirely net economic contribution. This is absolutely fine - gross impacts are still interesting, still matter and are a standard approach to economic modelling. However, it's important to interpret many of these induced jobs as "at risk" rather than guaranteed losses if the oil and gas sector shrinks.

The OEUK number of 220,000 is made up of 133,000 direct & indirect jobs and 86,000 induced jobs. The latest report does not break 133,000 down into direct and indirect.

So, how does this compare to official economic data?

Direct & Indirect jobs

The scope of which firms are included in "direct" jobs can vary. But the Oil and gas sector is generally thought to be made up of firms classified to industries “Extraction of crude petroleum and natural gas” and “Mining Support Services”. Official employment data from the Office for National Statistics' 2022 Business Register Employment Survey for these industries suggests that 11,000 people are employed in extraction (9,000 of which are in Scotland) and 17,000 are employed in mining support services (14,000 of which are in Scotland). So, this would suggest 28,000 people in the UK, 23,000 of which are in Scotland, are DIRECTLY employed in the oil and gas industry.

To estimate the indirect jobs, we can use the published Full-time equivalent (FTE) multipliers from the Office for National Statistics. The latest multipliers are for 2019, so bear this in mind: the supply chains may have changed since which could change the indirect numbers. But these multipliers suggest 150,000 direct and indirect jobs are supported across the UK from these industries.

This suggests that the total UK numbers presented by OEUK (which may well be influenced by more recent intelligence from industry) are in the right ballpark.

The extent to which these indirect jobs are in Scotland is slightly more difficult to estimate from published data. The Scottish Government have published an offshore satellite account (currently classified as experimental statistics, which should be borne in mind), which suggests that the offshore industry buys 3-4 times as much from onshore rest of UK than from onshore Scotland. In addition, comparing published Scottish multipliers to those produced by the ONS we can see the extent to which mining support services produce multiplier effects in Scotland vs the rest of the UK.

All of this allows us to estimate that the INDIRECT jobs in Scotland are likely to be around 35,000. Added to the direct jobs, this suggests around 58,000 jobs in Scotland directly and indirectly linked to the North Sea. (Interestingly / reassuringly, this is very close to an estimate of 57,000 produced in an independent report for the Scottish Government by EY recently).

Induced jobs

This leads us to the induced jobs. Firstly, there will be induced jobs generated from the direct and indirect jobs in Scotland (which is easy-ish to quantify) but also, there are likely to be induced jobs generated from direct and indirect jobs elsewhere in the UK.

From our models of UK and Scottish induced jobs, it would suggest that 90,000 jobs are induced in the UK as a whole. We estimate that, depending on how you allocate induced jobs to Scotland, between 8,000 and 26,000 of these could be in Scotland. As you can see, this is the area of most uncertainty, with these jobs being less directly linked to the oil and gas sector itself.

Our modelling suggests therefore that a total of around 66,000-84,000 would be a reasonable total for Scotland.

So, these numbers are very much in line with the OEUK numbers: and suggest, that IF indeed, half of North Sea jobs are at risk from plans to changes in investment allowances (which was the claim in the AGCC article) that probably 33,000 to 42,000 of the 100,000 at risk (again, if you are convinced by the claim) would be in Scotland.

This is, of course, still a very significant number of jobs. The important thing to take from this analysis is that the supply chains from direct jobs in oil and gas are likely to impact on jobs across the UK – so it is not just a Scottish issue.

The more important point

The AGCC represents many companies that are in or rely on the oil and gas sector. If, indeed, a policy could put investment at risk, it would be important to understand if it is likely to impact new investments as opposed to meaning that existing activity is under threat – which could change the extent to which certain numbers of jobs are at risk. In addition, jobs supported by a sector will not necessarily disappear if a sector does: the economy is dynamic, not static, and labour is likely to be reallocated to an extent.

The crucial thing for the North East of Scotland, though, is that many of these jobs are concentrated in a specific geographic area. And whilst we have said that induced jobs in particular may be supported by wage spending of other workers, we only need to look at the impacts we have seen on hotels and retail in Aberdeen since the oil price shock of 2015 to see that large reductions in oil and gas jobs could have a significant induced effect on other sectors in the region.

At the heart of all of this is a debate over the speed of the transition from oil and gas to other forms of energy, and how this can be done in a way that protects existing skills and supply chains that can be repurposed into new technologies.

In addition, there is a question about how we can grasp the opportunities that new technologies provide to develop new supply chains in areas where Scotland has strengths. The energy transition does have to happen, oil and gas will decline, and policymakers must look to see how investment can be unlocked in these new technologies to ensure the transition happens in a way that protects workers and communities.

There has been excellent research recently that looks into the pathways for transitioning workers and supply chains into new technologies.

A recent Rystad report, commissioned by OEUK, really helpfully specifies the relevant supply chains for each of the recent and new technologies, broken down into fixed bottom wind, floating offshore wind, hydrogen and Carbon Capture and Storage (CCS). It sets out, for example, that the relevant skills and supply chains for floating offshore wind are much more congruent with oil and gas skills and supply chains than fixed bottom wind. Another example is that it finds that we may have to protect our drilling skills and supply chain in the meantime if we are to take the opportunities that will come from CCS. This specificity for each of the technologies is what is required to allow policymakers to prioritise interventions to grasp the opportunities from the transition.

Another report, from Robert Gordon University's Energy Transition Institute, sets out the investment that is needed in new technologies to protect jobs over the next 6 years in particular, up to 2030. The point in this report is that IF this investment does not happen, then the government may have to take decisions around oil and gas (including new licences) to protect supply chains for when these new technologies come online.

Some will say that these sorts of claims from industry representatives are to be expected, and that similar things have been said in the past that have not transpired. As we see this issue being used as a political football in the election campaign, it is important not to make it about whether one is for or against the workers of the North East of Scotland – no one is against them, and everyone wants the economy to succeed.

The more important policy question is how different layers of government can work together to unlock investment in the transition as quickly as possible: whether that is about investment in grid connections, investment in skills or issues with the planning system. Some of the excellent research referenced can be used to help guide where policymakers could have most impact.

OEUK are releasing new numbers in a few weeks, so we can all look out for them to get the latest numbers for 2023.

Source - https://fraserofallander.org/are-there-thousands-of-jobs-at-risk-in-the-north-east-of-scotland/