GDP monthly estimate - UK December 2024

13th February 2025

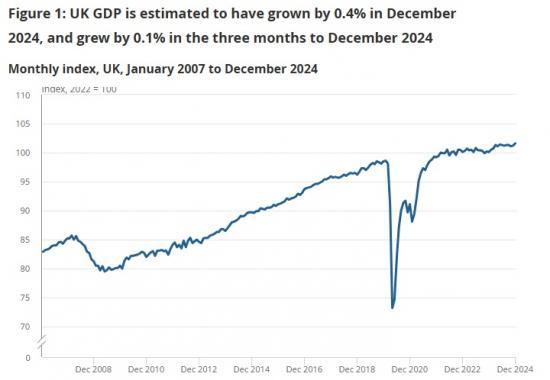

Monthly real gross domestic product (GDP) is estimated to have grown by 0.4% in December 2024, largely because of growth in the service sector, following an unrevised growth of 0.1% in November 2024.

Real GDP is estimated to have grown by 0.1% in the three months to December 2024, compared with the three months to September 2024, mainly because of growth in the services sector.

Monthly services output grew by 0.4% in December 2024, following growth of 0.2% in November 2024 (revised up from 0.1% growth in our previous publication), and grew by 0.2% in the three months to December 2024.

Production output grew by 0.5% in December 2024, following a fall of 0.5% (revised down from a fall of 0.4% in our previous publication) in November 2024; production fell by 0.8% in the three months to December 2024, driven by a decline in manufacturing output.

Construction output fell by 0.2% in December 2024, following growth of 0.6% (revised up from growth of 0.4% in our last publication) in November 2024, and grew by 0.5% in the three months to December 2024.

Annually, output GDP is estimated to have grown by 0.8% in 2024 compared with 2023.

The services sector

On the month, services output is estimated to have grown by 0.4% in December 2024, following growth of 0.2% in November 2024 (revised up from 0.1% growth in our previous publication). Of the 14 subsectors, output increased in eleven, with the remaining three subsectors seeing output decline in December 2024.

The largest positive contribution in the services sector in December 2024 came from the professional, scientific and technical activities subsector, where output rose by 1.2% during the month, following a fall of 0.5% in November 2024. Six out of the eight industries in this section experienced growth in December 2024, with the largest contribution coming from an increase of 3.4% in the advertising and market research industry.

The next largest positive contribution at the subsector level in December 2024 came from a 1.1% growth in administrative and support service activities, after two consecutive monthly declines in October and November 2024. The growth in December 2024 was mainly driven by office administrative, office support and other business support activities (up 1.9%); and travel agency, tour operator and other reservation service and related activities (up 3.3%).

The largest negative contribution in December 2024 came from information and communication which fell by 0.4%. This was driven by computer programming, consultancy and related activities, which fell by 1.3%, and publishing activities, which fell by 5.7%. This was partially offset by growth of 8.4% in the motion picture, video and TV programme production, sound recording and music publishing activities industry.

At the industry level, the largest positive contributions to services in December 2024 came from wholesale trade, except of motor vehicles and motorcycles (up 1.5%); motion picture, video and TV programme production, sound recording and music publishing activities (up 8.4%); and food and beverage service activities (up 2.0%). The largest negative contributions to the month came from computer programming, consultancy and related activities (down 1.3%); publishing activities (down 5.7%); and wholesale and retail trade and repair of motor vehicles and motorcycles (down 1.7%).

Overall, the services sector is estimated to have grown by 0.2% in the three months to December 2024, compared with the three months to September 2024. There was a rise in output in 8 of the 14 subsectors in this period.

The human health and social work activities subsector was the largest positive contributor to the rise in services output in this three-month period, growing by 0.9% in the three months to December 2024, compared with the three months to September 2024. The next largest contribution came from professional, scientific and technical activities, where output increased by 0.9%. The largest negative contribution during the three months to December 2024 was administrative and support service activities, which fell by 1.4%.

Consumer-facing services

Output in consumer-facing services increased by 0.4% in December 2024, following a revised growth of 0.6% in November 2024 (this figure was given as 0.5% growth in our previous bulletin). Food and beverage service activities was the largest contributor to the increase at the industry level, with output growing by 2.0%. This was followed by other personal service activities, where output increased by 2.8%. There was a fall of 1.7% in wholesale and retail trade and repair of motor vehicles and motorcycles in December 2024, which was the largest negative contributor to consumer-facing services in the month.

Consumer-facing services output rose by 0.1% in the three months to December 2024, compared with the three months to September 2024. The largest positive contributions in this period came from growth of 5.6% in the travel agency, tour operator and other reservation service and related activities industry. This was followed by other personal service activities, where output increased by 2.1%. The largest negative contribution was a fall of 0.8% in the retail trade, except of motor vehicles and motorcycles industry, in the three months to December 2024.

The production sector

On the month, production output is estimated to have grown by 0.5% in December 2024, following a revised fall of 0.5% in November 2024 (this figure was a fall of 0.4% in our previous bulletin). The December 2024 growth was a result of a 0.7% growth in manufacturing and a 1.5% growth in mining and quarrying. These growths were partially offset by a fall of 0.6% in electricity, gas, steam and air conditioning supply, and a 0.4% fall in water supply; sewerage, waste management and remediation activities in December 2024.

In the three months to December 2024, production output is estimated to have fallen by 0.8% when compared with the three months to September 2024, mainly because of a 0.7% fall in manufacturing over this period. There were also negative contributions from mining and quarrying, which decreased by 2.5% and electricity, gas, steam and air conditioning supply, which fell by 0.7% in the same period. These were partially offset by water supply; sewerage, waste management and remediation activities output, which increased by 1.2% in the three months to December 2024.

Manufacturing output grew by 0.7% in December 2024 and was the largest contributor to the growth in production output during the month, following a fall of 0.3% in November 2024. Manufacturing output increased in 7 of the 13 subsectors in December 2024. The largest positive contributions in December 2024 came from the manufacture of basic pharmaceutical products and pharmaceutical preparations (up 5.1%), following three consecutive monthly declines in this industry, and manufacture of machinery and equipment n.e.c. (up 5.9%). The largest negative contributions in November 2024 came from the manufacturing of computer, electronic and optical products (down 3.6%), and the manufacture of transport equipment (down 1.4%).

The construction sector

Monthly construction output is estimated to have fallen by 0.2% in December 2024, which follows an upwardly revised increase of 0.6% in November 2024 (this figure was given as 0.4% growth in our previous bulletin). The decrease in monthly output in December 2024 came solely from a fall of 1.8% in repair and maintenance, while new work grew by 1.1%.

Construction output is estimated to have grown by 0.5% in the three months to December 2024 compared with the three months to September 2024. New work increased by 1.2% over the period, whereas repair and maintenance fell by 0.4%. Within new work, the largest contributor to the increase came from private new housing, which grew by 1.3%. While the private new housing sector grew in the three months to December 2024, it still remains 20.4% lower than its highest post-coronavirus (COVID-19) pandemic level, recorded in the three months to September 2022.

In repair and maintenance, the largest negative contributor came from private housing repair and maintenance which fell by 2.5%.

Five out of the nine sectors saw decreases in December 2024. At the sector level, the main contributors to the monthly decrease were non-housing repair and maintenance and private housing repair and maintenance, which fell by 1.8% and 1.4%, respectively. Figure 8 shows both the monthly and three-monthly contributions to construction output from each of the construction sectors.

Annual Overview

On an annual basis, output gross domestic product (GDP) is estimated to have grown by 0.8% in 2024, this follows a growth of 0.4% in 2023. Services output was the largest contributor to growth in this period, increasing by 1.3%. Construction, and agriculture, forestry and fishing also both saw an increase in output in 2024, by 0.4% and 1.0%, respectively. These growths were partially offset by a 1.7% fall in production during the same period, with all four subsectors within production declining in 2024.

At industry level during 2024, twelve out of the twenty subsectors experienced growth, with the other eight industries falling during the period. The largest contributions to the growth came from professional, scientific and technical activities, which grew by 3.2% and human health and social work activities, which grew by 2.9% in 2024. The largest negative contribution came from mining and quarrying, which fell by 7.2% in 2024.

Read the full ONS report HERE