The Danger In A New Starter Home Deposit Loan Scheme

26th March 2026

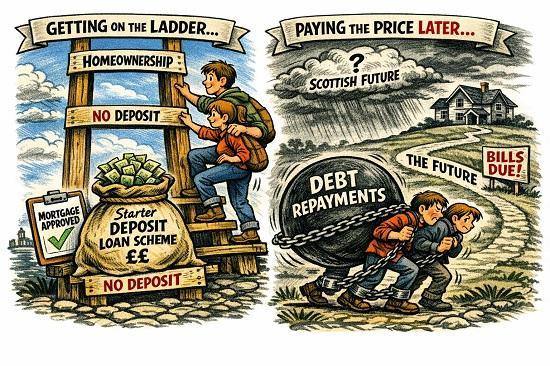

The Resolution Foundation's proposed deposit loan scheme shares structural similarities with student loans—delaying repayment until later in life but they warn this could create long-term debt burdens if not carefully designed. Like student loans, it risks becoming a deferred cost that weighs on future budgets, especially if interest rates rise or wages stagnate.

Rsolution foundation Deposit Loan Scheme

The Foundation explicitly cautions against repeating the mistakes of Help to Buy, which inflated prices by injecting credit into a supply-constrained market. Their scheme is more targeted—but the repayment model still echoes student loans, with the risk of future financial strain.

Risks That Could "Come Home to Roost"

Deferred burden: Young buyers may feel relief now, but face repayment pressure later—especially if wages stagnate or interest rates rise.

Cumulative debt

If combined with student loans, car finance, and other credit, the total repayment load could become unsustainable.

Housing market distortion

Even targeted schemes can nudge prices upward if supply remains tight, especially in areas like Aberdeen or the Highlands.

What Would Make It Safer?

The Foundation suggests safeguards:

Strict income-based eligibility to avoid over-lending

Cap on loan size to prevent runaway debt

Integration with housing supply policy to avoid price inflation

Transparent repayment terms to avoid future shocks

The deposit loan scheme could help renters transition to ownership—but only if paired with serious planning reform and clear repayment rules. Otherwise, it risks becoming a second student loan: a deferred cost that quietly shapes financial futures.