A Strong Start with Uncertain Momentum: What the UK's February 2026 GDP Report Really Shows

16th April 2026

The latest monthly GDP release from the Office for National Statistics offers a surprisingly upbeat snapshot of the UK economy in February 2026—though one that comes with clear warnings about what may lie ahead.

After a sluggish end to 2025 and a largely flat January, February delivered a marked shift in momentum, suggesting the economy entered the year on firmer footing than many had expected.

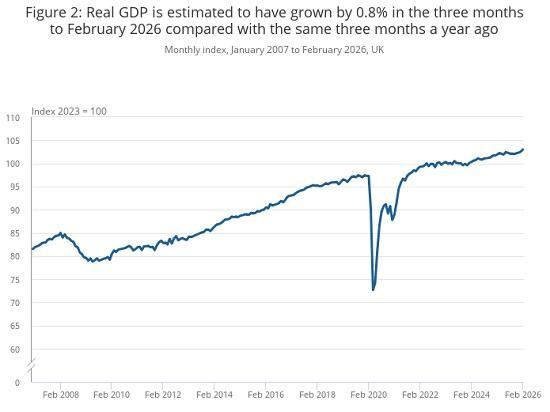

At the headline level, UK GDP grew by 0.5% in February 2026, a figure that significantly exceeded most forecasts and represents the strongest monthly expansion in over a year. This growth was not confined to a single part of the economy but was instead broad-based, with meaningful contributions from services, production, and construction.

The services sector, which dominates the UK economy, played a central role in driving this expansion. Activity increased across a range of industries, including wholesale trade, hospitality, and administrative services—areas closely tied to consumer demand and business activity. At the same time, the production sector also recorded growth, supported in part by a rebound in manufacturing output, particularly in the automotive industry following earlier disruptions. Meanwhile, construction output rose strongly, marking a recovery after previous declines and adding further weight to the overall expansion.

Looking beyond a single month, the broader trend also appears more encouraging. GDP rose by 0.5% over the three months to February, indicating that the improvement was not simply a one-off spike but part of a more sustained pickup in activity at the start of 2026.

However, while the February figures paint a positive picture, the report also sits within a more complex and fragile economic context. The strong growth came just before escalating geopolitical tensions—particularly disruptions affecting global energy markets—which are already expected to weigh on the UK economy in the months ahead. Rising oil and gas prices are likely to feed into higher inflation, increased costs for businesses, and reduced consumer spending power.

Economists have therefore been quick to caution against reading too much into a single strong month. Many view February's performance as a rebound from earlier weakness rather than the start of a sustained boom. Underlying challenges remain, including relatively weak investment, ongoing cost pressures, and sensitivity to global shocks. There are also concerns that growth could slow again in the second quarter of the year as these external pressures take hold.

In this sense, the February GDP report tells two stories at once. On the surface, it highlights a UK economy capable of stronger growth when conditions allow, with all major sectors contributing to expansion. Yet beneath that, it underscores how dependent that growth remains on stable global conditions and how quickly momentum can be undermined by external factors.

For businesses and policymakers alike, the message is clear: the UK entered 2026 with more resilience than expected, but that resilience is about to be tested. Whether February proves to be the start of a sustained recovery or merely a temporary high point will depend less on domestic performance and more on how the global economic environment evolves in the months ahead.

Read the full ONS report HERE