Trade Deficit Narrows but Imbalances Remain: What the UK's February 2026 Trade Data Tells Us

16th April 2026

The latest UK trade figures from the Office for National Statistics for February 2026 provide a cautiously encouraging picture of the country's external position.

But one that still highlights deep structural imbalances in how the UK trades with the world. While there are signs of improvement in the short term, the underlying dynamics of imports, exports, and sectoral dependence suggest that the UK’s trade challenges are far from resolved.

At the centre of the report is a narrowing of the UK’s overall trade deficit, continuing a trend seen in recent months. In the three months leading up to early 2026, the total trade deficit in goods and services shrank, driven by a combination of rising exports and a modest fall in imports. This suggests that UK businesses have been able to regain some momentum in international markets, while domestic demand for imported goods has softened slightly.

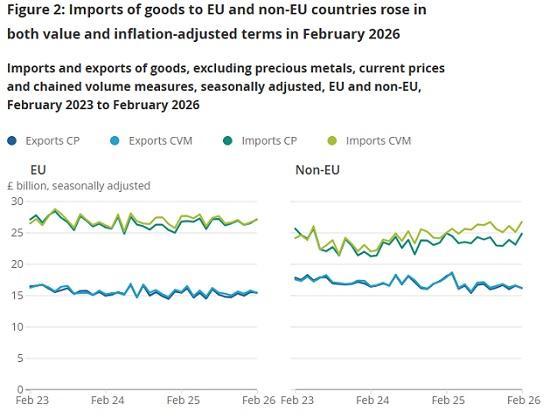

A key feature of the UK’s trade profile remains the stark contrast between goods and services. The UK continues to run a large deficit in goods trade, importing significantly more physical products than it exports. This reflects long-standing structural factors, including a relatively smaller manufacturing base and strong consumer demand for imported goods. At the same time, this weakness is partially offset by a strong surplus in services, particularly in sectors such as finance, professional services, and technology, where the UK remains globally competitive.

February’s data reinforces this pattern rather than changing it. Improvements in the overall trade balance are not coming from a revival in manufacturing exports alone, but from a combination of steady services performance and incremental gains in goods exports, alongside subdued import demand. In other words, the UK is not eliminating its trade deficit—it is managing it.

Another important dimension of the report is the three-month trend, which economists often view as more reliable than volatile monthly figures. Here, the narrowing of the deficit reflects a broader stabilisation in trade flows after a period of disruption in 2025. Export growth has been supported by stronger demand in some overseas markets, while imports have eased as domestic economic conditions remain relatively restrained.

However, this improvement comes with important caveats. The UK’s reliance on imports—particularly for energy, manufactured goods, and raw materials—means that its trade position remains vulnerable to global shocks. Recent geopolitical tensions and fluctuations in energy prices underline how quickly the balance can shift. A rise in import costs, for example, could easily widen the deficit again, even if export volumes remain stable.

There is also a question of sustainability. While services exports continue to perform strongly, they cannot indefinitely compensate for weaknesses in goods trade. The UK’s goods deficit has reached historically high levels in recent years, highlighting the scale of the structural gap.

Without a significant expansion in domestic production or a shift in consumption patterns, this imbalance is likely to persist.

From a policy perspective, the February trade data presents a mixed message. On one hand, the narrowing deficit suggests that the UK economy is becoming slightly more balanced in its external trade position. On the other, it underscores how dependent that improvement is on factors that may not be durable such as weaker import demand rather than a fundamental strengthening of export capacity.

In that sense, the report mirrors a broader theme across the UK economy in early 2026 short-term resilience masking longer-term challenges. The trade position is improving, but not transforming. For the UK to achieve a more sustainable external balance, future growth will likely need to come from stronger goods exports, increased investment in productive industries, and a continued expansion of high-value services.

Until then, the February figures should be seen not as a turning point, but as a temporary easing of pressure in a trade system that remains structurally imbalanced.