Inflation Isn’t Done Yet: Why Prices Are Creeping Back Up in Britain 3.3% Reported Today

22nd April 2026

For a while, it looked like the worst might be over.

After months of steady decline, inflation in the UK had begun to ease, raising cautious optimism that the cost-of-living squeeze was finally loosening. Prices were still high, but the pace of increase was slowing. There was a sense—fragile, but real—that things were moving in the right direction.

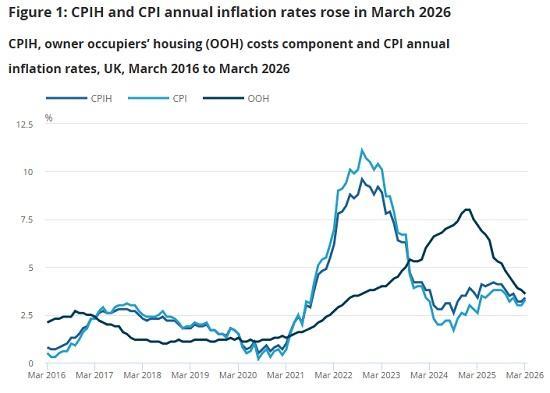

March 2026 has complicated that narrative.

The latest data shows inflation ticking back up to around 3.3%, reversing part of the recent progress. It’s not a dramatic surge, and it doesn’t signal a return to the double-digit rates of previous years. But it does highlight something more subtle and more concerning: inflation is proving stubborn.

This isn’t a story of broad-based price rises across the entire economy. Instead, it’s a story of pressure building in specific, critical areas—most notably energy.

Fuel and energy costs have once again become the driving force behind inflation. As global oil prices rise amid geopolitical tensions and supply uncertainty, the effects ripple quickly through the UK economy. Petrol and diesel become more expensive. Transport costs increase. Businesses face higher operating expenses. And those costs, sooner or later, are passed on to consumers.

It’s a familiar pattern, but one that underscores how exposed inflation remains to global shocks.

Elsewhere, the picture is more mixed. Food price inflation, which was once a major contributor to the cost-of-living crisis, has continued to stabilise. Some goods prices have also shown signs of easing. But these improvements are being offset by the renewed upward trends from energy and transport, creating an uneven and fragile overall trend.

What makes this moment particularly tricky is that inflation is no longer clearly falling but it’s not spiralling either. Instead, it’s hovering. Sticky. Resistant. Difficult to push down further without significant changes in either global conditions or domestic demand.

For policymakers, this presents a dilemma.

The Bank of England has been under pressure to begin cutting interest rates as economic growth remains weak. Lower rates could support borrowing, investment, and consumer spending. But rising inflation even modestly complicates that decision. Cutting too soon risks reigniting price pressures. Waiting too long risks stifling an already fragile economy.

It’s a balancing act with no easy answer.

For households, the implications are more immediate. Even small increases in inflation can delay relief. Prices may not be rising as rapidly as before, but they are still rising—and that means the overall cost of living continues to edge higher. For many, the push of financial pressure hasn’t disappeared; it has simply changed form.

The broader lesson from March’s data is that the path back to low, stable inflation was never going to be smooth. Global energy markets remain volatile. Supply chains are still sensitive to disruption. And the UK economy, like many others, is navigating a uneasy mix of domestic weakness and external shocks.

In that context, a slight uptick in inflation is less a surprise than a reminder.

A reminder that inflation doesn’t fall in a straight line.

A reminder that global events—from conflict to commodity prices—still matter deeply at the local level.

And a reminder that, even as the worst may be behind us, the journey back to stability is far from over.

For now, inflation in Britain isn’t surging. But it isn’t settling either.

And that uneasy middle ground may define the months ahead.

Read the full ONS report HERE