Inflation’s Warning Signal: A Sharp Surge in Producer Costs Beneath the Surface

22nd April 2026

Inflation doesn’t start in supermarkets or on high streets. It starts earlier inside factories, supply contracts, and supply chains. And the latest UK data suggests that, beneath the surface, something significant has shifted.

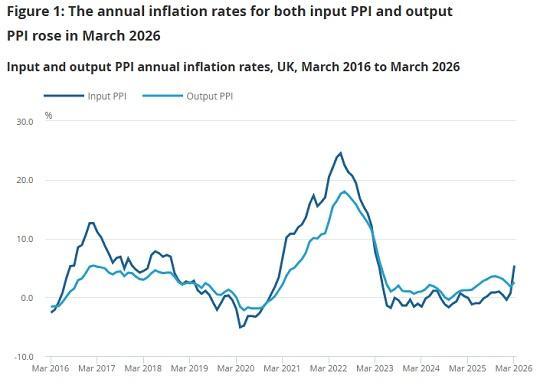

The newest figures on producer price inflation for March 2026 reveal a sharp and important change. Producer input prices surged by 5.4% in the year to March, up dramatically from just 0.7% in February. That is not a small fluctuation. It is a clear jump and one that signals renewed pressure building within the economy.

Input prices reflect what manufacturers pay for raw materials, fuel, and components. When those costs rise this quickly, businesses are forced to respond. They can absorb the increase and accept lower profits, or they can pass it on through higher prices. In reality, most do a combination of both but over time, those higher costs tend to feed through to consumers.

What makes this shift particularly notable is the speed of the change. Only a month earlier, input cost growth had been relatively subdued. The sudden acceleration suggests that underlying conditions—especially in energy and commodity markets—have turned.

Fuel is a major factor. Rising oil prices, driven by global uncertainty and supply disruption, have pushed up the cost of energy across the board. Because energy is a fundamental input into almost every stage of production and transport, increases here ripple quickly through the system. From manufacturing plants to delivery networks, higher fuel costs mean higher overall costs.

But energy is not the only pressure point. Materials and imported goods have also contributed, reflecting broader global cost increases. This combination creates a more persistent form of inflation one that is harder to reverse quickly.

Interestingly, the prices manufacturers charge for their goods—known as output or “factory gate” prices have not risen as sharply. This suggests that, for now, many businesses are absorbing some of the increased costs rather than passing them on immediately. But this gap rarely lasts. If input costs remain elevated, output prices tend to follow.

The inclusion of services in the latest data reinforces this concern. Service sector inflation is often slower moving but more persistent, driven by wages and operational expenses rather than volatile commodities. That means once price pressures take hold here, they can be harder to bring down.

Taken together, the data points to a key risk: while consumer inflation may appear relatively stable for now, the conditions for future increases are strengthening beneath the surface.

Producer price inflation is often described as a leading indicator—and for good reason. It shows where prices are heading before they get there. A sharp rise in input costs today can become higher shop prices tomorrow, especially if businesses begin to pass those costs along more aggressively.

For policymakers, this creates a difficult balancing act. On one hand, inflation at the consumer level has not surged dramatically. On the other, the pipeline feeding into it is heating up again. Acting too slowly risks allowing these pressures to build; acting too quickly risks damaging an already fragile economy.

For businesses, the challenge is immediate and practical. Rising costs squeeze margins and force difficult decisions on pricing, investment, and hiring. For consumers, the impact may not be immediate but it is likely coming.

The March 2026 data delivers a clear message. The recent calm in inflation may not signal the end of the problem. Instead, it may be a pause—one that is now giving way to renewed pressure.

Because in the world of inflation, what happens behind the scenes rarely stays there for long.

Read the full ONS report HERE