Borrowers left in limbo as mortgage rates shift again

27th April 2026

Borrowers are in limbo once again, yet any hold to the Bank of England Base Rate (BBR) must not deter them from seeking a deal, according to Moneyfactscompare.co.uk analysis.

Mortgage market analysis

The biggest high street banks have all moved to cut selected fixed rates over the past two weeks, which includes Barclays, HSBC, Lloyds Bank, NatWest and Santander, all catching up to swap rate movements. Whether further cuts continue is up for debate.

Market expectations for interest rates to be higher for longer drove lenders towards hiking mortgage rates. The Moneyfacts Average Mortgage Rate noted its biggest monthly rise since July 2023. During the summer of 2023, the mortgage market felt a huge shock, when markets priced in higher rates for longer, due to stubbornly high inflation.

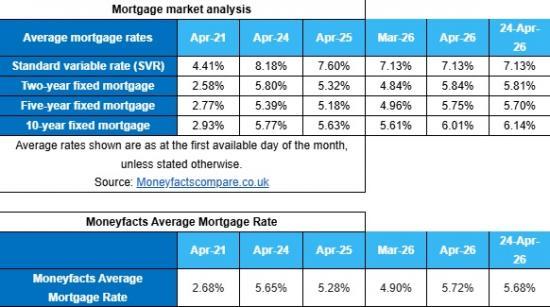

Year-on-year, average mortgage rates across the two-, five- and 10-year fixed sector have all risen. As of the start of April, the average 10-year fixed breached 6% for the first time since July 2024. The average two-year fixed rate reached its highest point since July 2024, and the five-year equivalent rose to its highest point since November 2023.

The Bank of England Base Rate was cut to 3.75% in December 2025, since then, the average standard variable rate (SVR) has fallen by 0.14%, from 7.27% to 7.13%. Year-on-year, BBR has fallen by 0.75%, but the average SVR has fallen by just 0.47%.

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, said, “Borrowers have been left in limbo as it is difficult to know whether they should rush to lock into a fixed deal or wait and see if lenders make more sizeable cuts. Unfortunately, the outlook on interest rates remains uncertain, so mortgage holders coming off a cheap fixed rate will have to cover higher repayments this year, which will be incredibly frustrating. It is still worth moving off an expensive revert rate, as borrowers could save almost £2,500 a year moving onto a fixed rate deal*.

“The Bank of England refuses to rush any decisions, and with fears of a recession already creeping in, it looks like stagflation has thrown out any plans for cuts this year. Economists expect the BOE base rate to hold in the short-term, and it’s looking increasingly unlikely we will see a cut until 2027. However, borrowers will hope that the mortgage mayhem experienced over recent weeks will calm, but repricing could go both ways amid swap rate moves. Mortgage rate hikes have been driven by the conflict in the Middle East, where the disruption of supply chains has created muddied waters for the future path of inflation and interest rate setting.

“Increasing pressures on households have the potential to echo the shocks felt by the UK during the summer of 2023, so the biggest concern for consumers will be how long they need to endure it, particularly for those looking to buy a home or remortgage, as mortgage rates have risen significantly in a short space of time. The Moneyfacts Average Mortgage Rate rose by 0.82% month-on-month (1 March versus 1 April), the biggest monthly rise since July 2023 of 0.83% (1 June versus 1 July). While the spikes in rates look similar on the surface to the shocks felt in the summer of 2023, and not forgetting the mini-Budget in 2022, they have very different driving forces.

“Lenders will be watching the decision by the Monetary Policy Committee (MPC) very closely, as it would be unwise to price deals too low in the short-term, so they will react if swap rates start rising significantly again. At the end of February, before the unrest in the Middle East began, the biggest banks (Barclays, HSBC, Lloyds Bank, NatWest and Santander) had their lowest two-year fixed mortgages priced around 0.30% above the two-year swap rate of 3.33%**, but back then there were also expectations for more BOE base rate cuts. This is why borrowers had a decent pool of sub-4% fixed deals to choose from. Base rate tracker mortgages currently look attractive but could be a gamble if interest rates rise this year, so choosing a deal with no early repayment charge would be wise.

“Lenders will be looking to reprice to catch up to higher swap rates over the coming days, but also to compete for new business, it’s all in the margins. Until the market sees more stability, there is very little scope for lenders to drop rates substantially due to the prolonged unrest in the Middle East. Any borrower concerned about securing a mortgage would be wise to seek advice from a broker to navigate the mortgage maze.”

*Average standard variable rate (SVR) is currently 7.13%. Calculations based on a £250,000 mortgage over a 25-year term on a repayment basis. SVR repayment £1,787 per month, versus £1,581 per month on 5.81% two-year fixed rate, monthly difference of £206, which is £2,472 over 12 months.

**On 27 February 2026, two-year swap was 3.33%, five-year swap rate was 3.51% - Moneyfacts onescreen. Lowest two-year fixed mortgage deals that were available direct to consumers and not tied to a current account: Santander – 3.51%, HSBC – 3.61%, NatWest – 3.62%, Lloyds Bank – 3.66% and Barclays Mortgage – 3.70%. The average of these low rates is 3.62% – which is 0.29% higher than the two-year swap of 3.33% on 27 February 2026.

The lowest rates as of 24 April 2026: Lloyds Bank – 4.55%, Barclays Mortgage – 4.60%. HSBC – 4.65%, NatWest – 4.65% and Santander – 4.70%. The average of these low rates is 4.63% – which is 0.33% higher than the two-year swap of around 4.30% on 24 April 2026.