High Street Under Pressure: Which Food Businesses Are Most Likely to Disappear and Which Will Survive

2nd May 2026

Across the UK, the high street is entering a period of quiet but significant change. Rising energy costs, strained supply chains, and shifting consumer habits are combining to reshape the economics of everyday food businesses.

While there is no single moment of collapse, the pressures are uneven and that unevenness is beginning to determine which businesses are most at risk, and which are likely to endure.

At the heart of the issue is cost. Energy prices affect nearly every part of the food economy: cooking, refrigeration, transport, and raw ingredients. When these costs rise together, businesses that operate on thin margins or rely heavily on energy-intensive processes find themselves exposed. The result is not always immediate closure, but a gradual tightening—reduced hours, smaller menus, higher prices, and, in some cases, eventual exit from the market.

This pressure is set to intensify with the upcoming increase in the UK energy price cap, regulated by Ofgem.

From 1 July, the cap is expected to rise again, pushing up electricity and gas bills for households and, indirectly, for businesses as well. While the cap technically applies to domestic users, its effects ripple through the economy: suppliers, landlords, and small business owners all face higher underlying energy costs. For food businesses already operating close to the edge, this “uplift” acts as an additional squeeze at precisely the wrong moment—when margins are already under strain from fuel and supply issues.

Among the most vulnerable are traditional takeaway models built around high energy use and narrow margins. The classic fish and chips shop is a clear example. These businesses depend heavily on deep frying, which requires constant high heat, and on ingredients like fish that are themselves tied to volatile fuel costs through the fishing industry. When boats stay in port because diesel is too expensive, supply shrinks and prices rise.

Even if chip shops pivot to sausages or pies, they often lose their most profitable product and face the same rising costs across oil, potatoes, and utilities. Over the next year, some of the weakest operators in this category particularly independents without strong local followings—are likely to disappear.

A similar vulnerability affects other energy-intensive formats.

Fried chicken outlets, small bakeries running ovens all day, and fast-paced kitchens using techniques like stir frying all face relentless input costs. These businesses cannot easily reduce their energy use without changing the product itself. When combined with price-sensitive customers, this creates a difficult balancing act: raise prices too much and demand falls; absorb the costs and margins vanish. It is in this space that closures are most likely to occur quietly and steadily.

Low-margin, high-volume businesses more broadly are under strain. Independent cafés, budget takeaways, and small family-run outlets often lack the financial cushion to absorb prolonged cost increases. They also tend to have limited negotiating power with suppliers and less ability to spread risk. The July price cap increase will likely accelerate this pressure, as even small rises in overheads can tip fragile businesses from survival into loss. Over time, this makes them particularly vulnerable to sustained inflation in energy and ingredients. The coming year is likely to see a continued thinning of this segment, especially in areas with high rents or heavy competition.

However, not all parts of the high street face the same outlook.

Businesses with flexible menus occupy a more stable middle ground. Many takeaways—serving dishes such as chow mein or chicken tikka masala—can adjust ingredients, portion sizes, or menu emphasis in response to changing costs. If one protein becomes expensive, another can be promoted; if portions shrink slightly, prices can be held. These adaptations are rarely visible in isolation, but collectively they allow such businesses to remain viable. While they are not immune to rising costs, they are less likely to disappear outright.

At the more resilient end of the spectrum are businesses with either pricing power or structurally lower exposure to energy costs. Premium restaurants, for example, can often pass on higher costs to customers who are less sensitive to price increases. Their margins, while not immune, provide more room to manoeuvre. Similarly, cafés and delis that focus on sandwiches, salads, and other low-energy foods benefit from reduced reliance on constant high-heat cooking. Their cost base, while still rising, is less directly tied to fuel-intensive processes.

Large chains and franchises also hold a significant advantage. With bulk purchasing agreements, established supply networks, and greater financial reserves, they can absorb shocks that would overwhelm smaller competitors. Over time, this may lead to a subtle shift in the composition of the high street, with independent outlets giving way to more standardised, chain-based operations.

The broader pattern that emerges is one of selection rather than collapse.

Businesses that are highly energy-dependent, narrowly focused, and operating on thin margins are most at risk—especially as additional pressures like the July energy price cap increase take effect. Those that are flexible, better capitalised, or less reliant on intensive cooking methods are more likely to survive—and in some cases, expand into the gaps left behind.

For consumers, the changes may appear gradual with a favourite takeaway closing, prices creeping up, menus simplifying. But taken together, these shifts point to a deeper transformation. The high street is not disappearing. It is adapting. Over the next year, it will likely become leaner, more consolidated, and shaped increasingly by businesses that can navigate an environment where energy, more than ever, defines what is possible.

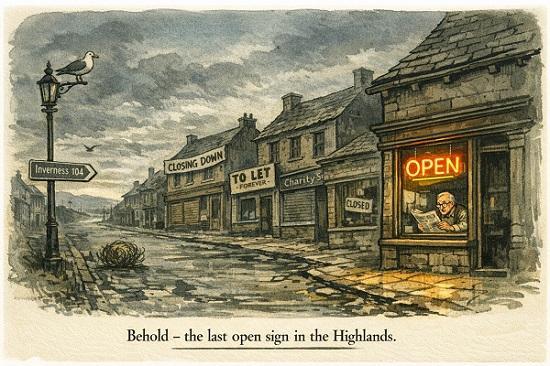

Yet this latest wave of pressure is landing on a high street that was already weakened. Over the past decade, many UK towns have seen a steady erosion of shops due to earlier financial strains—rising rents, the growth of online retail, changing consumer habits, and the aftershocks of economic crises. Empty units, reduced footfall, and fragile business ecosystems were already part of the landscape.

What is happening now is less a new crisis than an intensification of an existing one. In that sense, the current energy and cost pressures are accelerating a longer-term trend. A gradual reshaping of the high street, where only the most adaptable, well-supported, or well-positioned businesses are likely to remain.