Rising UK Government Borrowing Costs: Causes and Consequences

6th May 2026

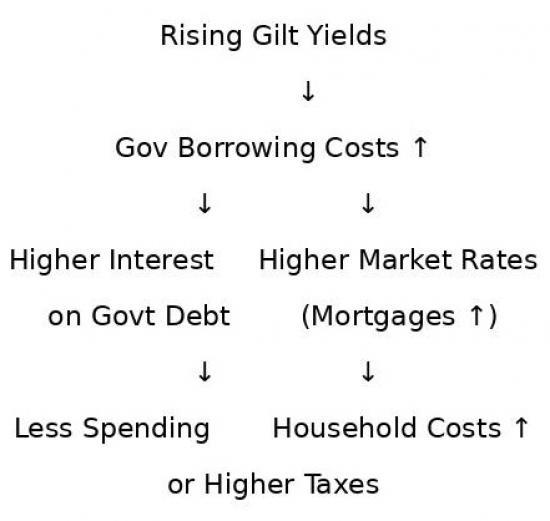

In recent weeks, the cost of borrowing for the UK government in the bond market has risen sharply, reaching levels not seen in decades. These costs are reflected in the yields on UK government bonds, known as “gilts.” When gilt yields rise, it means the government must pay more interest to borrow money. This shift has important implications not only for government finances but also for the wider economy and ordinary citizens.

A Trend with a Sharp Acceleration

The increase in borrowing costs has not been a single sudden upsurge but rather a sustained upward trend that has recently accelerated. Over the past month, gilt yields had already been climbing due to a combination of economic and political concerns. However, on 5 May 2026, there was a noticeable jump: long-term yields rose by roughly 0.1–0.15 percentage points in a single day, pushing 30-year borrowing costs to their highest level since the late 1990s.

While such a move might seem small, in bond markets it is significant—especially for long-term debt. This means that although the rise was gradual overall, certain days like 5 May acted as “trigger points,” where new information or heightened uncertainty caused investors to rapidly reassess the risks of lending to the government.

Why Have Borrowing Costs Increased?

Several interconnected factors explain this rise.

First, inflation expectations have played a major role. Concerns about rising energy prices and broader inflationary pressures have led investors to demand higher returns to compensate for the erosion of purchasing power over time. If inflation remains high, the real value of future interest payments falls, so lenders insist on higher nominal yields.

Second, expectations about interest rates set by the Bank of England have shifted. Markets increasingly believe that interest rates will remain elevated for longer, or may even rise further. Since bond yields tend to track expected future interest rates, this has pushed gilt yields upward.

Third, political and fiscal uncertainty has contributed to the increase. Investors are wary about the UK’s fiscal outlook, including the possibility of higher government borrowing in the future. Political developments—such as election uncertainty or concerns about policy direction—can raise doubts about how public finances will be managed, leading investors to demand a higher “risk premium.”

Finally, the sheer scale of government borrowing matters. The UK is expected to issue a large volume of debt, and when supply increases significantly, yields can rise unless there is sufficient demand to absorb it. In simple terms, if more bonds are being sold, they may need to offer higher returns to attract buyers.

Implications for Government Spending

Higher borrowing costs place direct pressure on government finances. As new debt is issued at higher interest rates and older debt is refinanced, the total cost of servicing the national debt increases. This means a larger share of tax revenue must be devoted to interest payments.

As a result, the government faces a tighter fiscal environment. There is less “headroom” for additional spending, tax cuts, or investment projects. Policymakers may be forced to make difficult choices, such as reducing planned expenditure, increasing taxes, or delaying new initiatives. In this way, financial markets can exert a form of discipline on government policy.

Affects on Ordinary Citizens

Although government bond markets may seem distant from everyday life, rising borrowing costs can affect ordinary people in several important ways.

One of the most immediate channels is through interest rates more broadly. Higher gilt yields tend to push up borrowing costs across the economy, including mortgage rates. For homeowners with variable-rate mortgages or those seeking to remortgage, this can mean significantly higher monthly payments.

Second, public services may come under pressure. If more government revenue is spent on debt interest, there is less available for areas such as healthcare, education, and infrastructure. This can lead to slower improvements, spending cuts, or reduced service quality over time.

Third, taxation may be affected. To manage higher debt costs, governments may choose to raise taxes or avoid planned tax cuts. This can reduce disposable income for households.

Fourth, economic growth could be impacted. Higher borrowing costs can dampen investment by both the government and private sector. Slower growth can translate into weaker wage increases, fewer job opportunities, and a generally more challenging economic environment.

Finally, pensions and savings can also be influenced. On one hand, higher yields can benefit savers by increasing returns on certain fixed-income investments. On the other hand, volatility in bond markets can affect pension funds and financial markets more broadly, creating uncertainty about long-term returns.

The Nitty Gritty

The recent rise in UK government borrowing costs reflects a combination of inflation concerns, interest rate expectations, political uncertainty, and increased debt issuance. While the upward movement has been gradual overall, specific moments—such as the jump on 5 May highlight how quickly market sentiment can shift.

The consequences extend beyond government finance. Higher borrowing costs constrain public spending and ripple through the wider economy, affecting mortgages, taxes, public services, and economic growth. For ordinary citizens, this means that movements in the bond market though often overlooked can have tangible and lasting effects on everyday financial life.