Why Westminster Chaos Is Pushing Up Caithness Mortgage Bills

13th May 2026

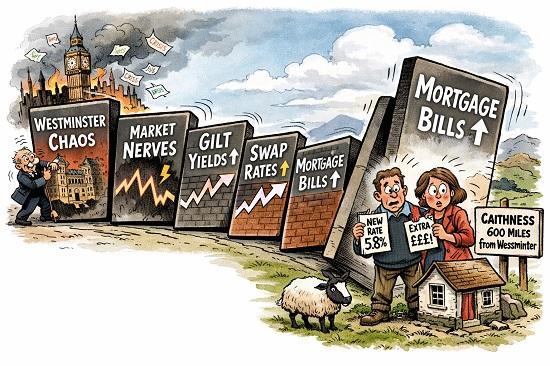

Political drama in London might feel distant from Wick or Thurso, but it has a direct line into your mortgage payments. Every bout of instability in Westminster such as leadership speculation, fiscal uncertainty, election noise sends a ripple through financial markets. By the time that ripple reaches Caithness, it shows up as higher mortgage rates, fewer deals, and rising monthly costs.

Political instability makes investors nervous

When markets sense uncertainty, they demand higher returns to lend to the UK. That pushes up gilt yields — the government’s borrowing costs. Gilt yields are the foundation of mortgage pricing, so when they rise, lenders reprice mortgages upward.

This happens even if the Bank of England keeps the base rate frozen.

Higher gilt yields mean higher mortgage rates

Most UK mortgages are fixed‑rate, and lenders hedge them using financial contracts tied directly to gilt yields. When political instability pushes those yields up, lenders’ costs rise — and they pass that cost straight to borrowers.

That’s why mortgage rates have risen several times this year without a single Bank Rate increase.

Caithness feels the squeeze more sharply

The Far North always pays more for national instability:

Fewer lenders operate locally

Lower incomes make affordability tighter

Higher living costs (fuel, food, heating oil) leave less room for mortgage shocks

Older housing stock means higher running costs

A 0.5% rise in mortgage rates hits a Caithness household harder than one in the Central Belt.

What this means for 2026

Unless political stability returns, Caithness households should expect:

mortgage rates to stay elevated

lenders to keep withdrawing and repricing deals

remortgaging to remain expensive

first‑time buyers to face tougher affordability tests

In short: Westminster turbulence becomes a real‑world financial squeeze in the Far North.