The World Is Running Short of Refineries And Scotland Is Feeling It First

13th May 2026

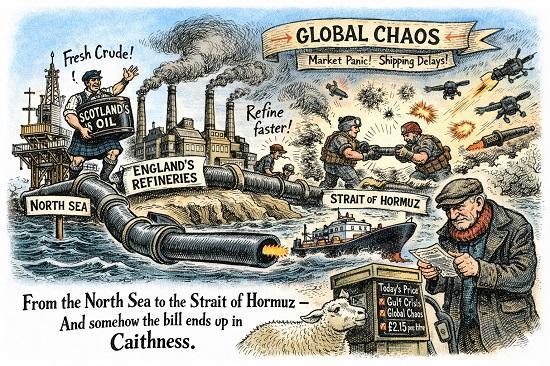

For most of the past century, the global oil system was built on one assumption. Crude oil would always be plentiful, refineries would always be running, and tankers would always be able to move freely.

That assumption has now collapsed. Over the last decade, the world has quietly shut down a significant share of its refining capacity — the industrial heart that turns crude oil into petrol, diesel, jet fuel and heating oil. Then came two wars: Russia’s invasion of Ukraine, and the Gulf conflict that has disrupted tanker routes through the Strait of Hormuz. What had been a slow‑burn structural problem suddenly became a global vulnerability.

The UK, and Scotland in particular, are discovering this the hard way. The closure of the Grangemouth refinery which was Scotland’s only refinery has turned a long‑standing strategic weakness into an immediate risk.

A country that produces oil in the North Sea now imports almost all of its refined fuels. And in places like Caithness, where every supply chain is stretched by distance, weather and transport fragility, the consequences are sharper than anywhere else.

The slow unravelling of global refining capacity

Refineries have been closing across the world for years, but the pattern was easy to ignore. In Europe, ageing plants struggled with high upgrade costs and tightening environmental rules.

In the United States, several refineries shut down or converted to biofuel production after the pandemic collapse in demand. Australia lost most of its refining sector entirely. South Africa’s refineries went offline after safety failures and never returned. Even in Asia, where demand is still rising, Japan and South Korea have been rationalising older plants.

The result is a world that still produces plenty of crude oil, but has far less capacity to turn it into usable fuels. This is the real bottleneck and it is why global markets have become so sensitive to disruption. When a refinery closes, it is not easily replaced. These are multi‑billion‑pound facilities that take years to build and decades to pay off. Once gone, they rarely return.

Two wars exposed the fragility

The Ukraine war was the first shock. Russian refineries were some of the largest suppliers of diesel to Europe and became targets for Ukrainian drone strikes. Europe banned Russian refined products, forcing long‑distance imports from India, the Middle East and even China. Tanker routes lengthened, shipping costs rose, and the global diesel market tightened.

Then came the Gulf conflict. Iran’s attacks on tankers and its intermittent blockade of the Strait of Hormuz disrupted the flow of Middle Eastern fuels. Insurance costs soared. Several tankers diverted around Africa, adding weeks to journey times. The UK received what was described as its “last shipment of jet fuel from the Gulf” before the route became too risky. Suddenly, the world’s shrinking refinery network was being asked to supply the same demand through longer, more dangerous routes.

This is the context in which Scotland shut down Grangemouth.

The loss of Grangemouth — and why it matters now

Grangemouth was not just another industrial site. It produced almost all of Scotland’s aviation fuel, supplied petrol and diesel across the central belt, and provided resilience for northern England. It was the last piece of Scotland’s refining infrastructure — a country that once had multiple refineries and a thriving petrochemical sector.

Its closure, announced in 2023 and completed in 2025, was justified on commercial grounds. The owners argued that the refinery was uncompetitive, required major investment, and could not survive in a world moving toward electrification. But the timing could not have been worse. The UK now has only four refineries left, down from more than a dozen in the 1990s. Scotland has none.

In a stable world, this would be a strategic inconvenience. In a world of tanker disruptions, refinery shortages and geopolitical conflict, it is a structural vulnerability.

What this means for Caithness fuel prices

For Caithness, the loss of Grangemouth is not an abstract national issue it is a direct contributor to higher pump prices and greater volatility. Every litre of petrol and diesel now travels further, through more intermediaries, and with more exposure to global shipping risks. The Highlands already pay a rural premium due to distance, low turnover and limited competition. Add global refinery tightness and tanker disruption, and the price gap widens.

When global markets tighten, the impact is felt first and hardest at the edges of the network. Caithness is the edge. A delay at a terminal in the central belt can ripple north within days. A spike in global diesel prices can show up at Wick or Thurso faster than in London, because rural suppliers have less ability to absorb shocks.

In short the loss of domestic refining amplifies every global tremor, and Caithness feels the tremors first.

Aviation fuel security for Inverness and Wick

Aviation fuel is even more exposed than road fuel. Before closure, Grangemouth supplied 97% of Scotland’s jet fuel. Now every drop must be imported. Inverness Airport, and any future operations at Wick John O’Groats Airport, depend entirely on tanker deliveries from distant refineries.

In normal times, this is manageable. In a crisis, it becomes a choke point. A single delayed shipment, a storm‑closed port, or a tanker diversion could leave airports short. For Wick already fighting for scheduled services the loss of local refining removes one more layer of resilience. For Inverness, it means higher costs and greater vulnerability during global disruptions.

The irony is stark: Scotland produces oil offshore, but must import the fuel needed to fly its own planes.

What a UK “fuel resilience plan” would actually require

Politicians often talk about “energy security”, but rarely distinguish between electricity, gas and refined fuels. The UK has plans for electricity resilience and gas storage. It has no equivalent plan for petrol, diesel or jet fuel — the lifeblood of transport, agriculture, emergency services and aviation.

A real resilience plan would require several elements. First, strategic fuel reserves — not just crude oil, which the UK already holds under international obligations, but refined products stored in multiple regions. Second, protected import routes, including diversified suppliers beyond the Gulf. Third, investment in domestic refining or at least modular refining capacity that can be activated in emergencies. Fourth, a recognition that rural areas like the Highlands need priority planning, because they are the first to be cut off and the last to be restored.

Without such a plan, the UK is exposed. Scotland is more exposed still. And Caithness — at the end of the longest supply chain in Britain — is the most exposed of all.

The uncomfortable conclusion

The world is not running out of oil. It is running out of refineries, stable shipping routes and geopolitical calm. The closure of Grangemouth did not cause this crisis, but it removed Scotland’s last buffer against it. In a world where wars disrupt tankers and refineries are scarce, the UK’s decision to rely almost entirely on imported fuels looks increasingly reckless.

For Caithness, the stakes are clear. Higher prices, greater volatility, and a supply chain that depends on events thousands of miles away. The Highlands have always lived with distance. What they now live with is fragility — a fragility created not by geography, but by policy choices made far from Wick, far from Inverness, and far from the communities that will feel the consequences first.