When the UK Grows but Caithness Stands Still: What the Latest GDP Figures Really Mean for the Far North

14th May 2026

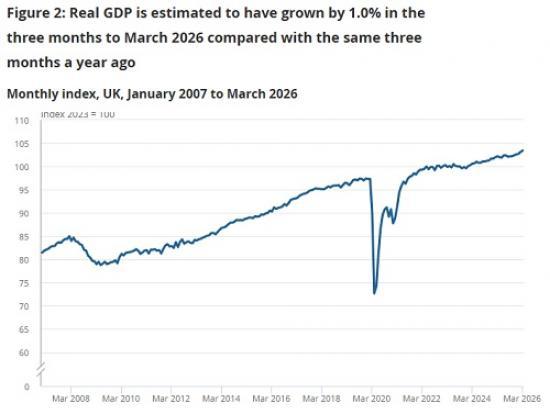

The latest GDP figures from the Office for National Statistics paint a picture of a UK economy that is moving — slowly, unevenly, and with more fragility than confidence. March 2026 delivered a modest 0.3% rise in GDP, with a 0.6% increase over the three‑month period.

On paper, this looks like progress. But as ever, the national averages hide the regional realities, and nowhere is that gap more visible than in Caithness and the wider Highlands.

The headline story is that services continue to carry the UK economy. Eleven out of fourteen service subsectors grew, from retail to IT to professional services. This is the kind of growth that flatters the national picture but does little for areas like Caithness, where the service sector is smaller, more fragile, and more exposed to seasonal and demographic pressures.

When London’s digital firms expand or Manchester’s professional services boom, it shows up in the GDP figures. When a shop closes in Wick or a hospitality business in Thurso struggles through another quiet shoulder season, it barely registers.

Production, meanwhile, is losing momentum. Manufacturing managed a respectable rise, but the wider production sector fell in March, dragged down by electricity, gas, and extractive industries. For the Highlands, where energy infrastructure, grid constraints, and transmission costs already shape daily life, this decline is more than a statistical footnote. It signals volatility in the very sectors that underpin rural resilience. When energy output dips, prices and uncertainty tend to rise — and the further you live from the Central Belt, the more you feel it.

Construction offers a glimmer of hope, with a 1.5% rise in March and a 0.4% increase over the quarter. But even here, the picture is mixed. New housing work remains weak, and private housing — the backbone of rural construction — is still struggling.

Caithness knows this story all too well: a shrinking pool of tradespeople, rising material costs, and a planning system that moves at a pace entirely unsuited to rural need. A national uptick does not translate into more homes being built in Lybster or more repairs being carried out in Reay. It simply means the sector has stopped falling — for now.

The ONS also highlights the economic ripples from the Iran conflict, which began in late February. Businesses across the UK reported mixed effects, but the pattern is familiar: supply chain uncertainty, rising costs, and a tendency to bring forward activity to avoid future price spikes.

The surge in fuel sales in March — motorists stocking up before expected increases — is a reminder of how quickly global events hit local wallets. In Caithness, where every journey is longer and every delivery more expensive, these shocks land harder and linger longer.

Real‑time indicators for April suggest that the fragility continues. Retail footfall is flat. Fuel prices are up 12%. Businesses reporting falling turnover have risen from 23% to 27%. New car registrations are down sharply from March. These are not the signs of an economy gaining strength; they are the signs of one trying to keep its balance on shifting ground.

For Caithness, the message is clear. The UK may be edging forward, but the benefits are not evenly shared. Growth concentrated in urban services does little for a region where distance, demography, and decades of centralisation have hollowed out the economic base. The national narrative speaks of recovery. The local experience is one of resilience — the quiet, unglamorous kind that keeps communities going despite the odds.

GDP may be rising, but the lived reality in the Far North remains shaped by factors the national figures barely acknowledge: the cost of fuel, the fragility of supply chains, the struggle to recruit, the slow erosion of services, and the long distances that turn every price rise into a heavier burden.

Until economic policy recognises that rural Scotland operates on a different set of fundamentals, Caithness will continue to watch the national numbers climb while wondering when — or if — the benefits will ever reach the edge of the map.

Main points from the ONS report 14 May 2026

In the three months to March 2026, compared with the three months to December 2025:

Real gross domestic product (GDP) grew by 0.6%, following a growth of 0.5% in the three months to February 2026 and a growth of 0.4% in the three months to January 2026 (revised up from a growth of 0.3% in our previous publication).

Services output grew by 0.8%, after showing a growth of 0.6% in the three months to February 2026 (revised up from a growth of 0.5% in our previous publication).

Production output grew by 0.2%; this follows a growth of 1.1% in the three months to February 2026 (revised down from a growth of 1.2% in our previous publication).

Construction output grew by 0.4%, following five consecutive three-monthly falls, including the three months to February 2026 falling by 1.9% (revised up from a fall of 2.0% in our previous publication).

In the month to March 2026:

Monthly GDP grew by 0.3% in March 2026, following a growth of 0.4% in February 2026 and no growth in January 2026 (revised down from growths of 0.5% and 0.1%, respectively, in our previous publication).

Services and construction output both grew, by 0.3% and 1.5%, respectively - these growths were partially offset by a 0.2% fall in production.

Read the full ONS report HERE