Pound Falls As Government Debt Interest Soars

15th May 2026

As of mid‑May 2026, the pound has weakened noticeably and UK borrowing costs remain elevated.

The pound has lost roughly 1½ % in May and about ¾ % since January, trading near the lower end of its recent range. Analysts expect it could slip toward $1.30 by June if global risk aversion rises.

UK government borrowing costs

10‑year gilt yield: ≈ 5.1 %

30‑year gilt yield: ≈ 4.9 %

2‑year gilt yield: ≈ 5.2 %

These are the highest sustained levels since 1998, reflecting persistent inflation and investor caution.

Higher yields mean the Treasury now pays around £5 million a year in interest for every £100 million borrowed, compared with roughly £2 million a year two years ago.

⚙️ Why it matters

Rising gilt yields → higher government borrowing costs → pressure on public finances and councils.

A weaker pound → dearer imports → renewed inflation risk → Bank of England less likely to cut rates soon.

Together, these trends keep UK interest rates and mortgage costs elevated and make new public borrowing more expensive.

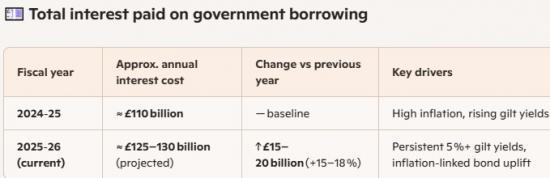

As of mid‑May 2026, the UK government’s debt‑interest bill has surged sharply compared with last year — driven by higher gilt yields and inflation‑linked payments.

That means the Treasury is now spending about £1 in every £8 of tax revenue on debt interest — roughly double the share seen before the 2022 mini‑budget crisis.

Why it’s higher

Gilt yields remain around 5 %, compared with 4.2 % a year ago.

Index‑linked gilts (about 25 % of UK debt) rise automatically with inflation, adding billions.

Short‑term refinancing costs more as older, cheaper debt matures.

Implications

Each 1 % rise in average borrowing cost adds roughly £25 billion to annual interest payments.

Councils and public bodies tied to Treasury rates — including Highland Council — face higher financing costs for capital projects.

The UK’s debt‑interest bill is now larger than the education budget and close to defence spending.