UK Inflation Falls Again as Energy Bills Drop but Fuel Prices Surge April 2026 ONS CPI Report

20th May 2026

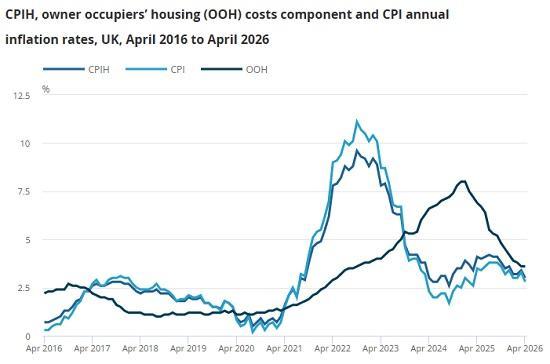

The April 2026 inflation figures mark another step in the UK’s slow return toward price stability.

According to the latest ONS release, both headline measures—CPIH and CPI—fell for the second consecutive month, driven largely by reductions in household energy bills.

Yet the picture is far from uniform as a sharp spike in petrol and diesel prices created the single largest upward pressure on inflation, highlighting the fragility of the UK’s cost environment.

Headline Inflation: A Gradual Descent

CPIH rose 3.0% in the 12 months to April 2026, down from 3.4% in March. CPI followed the same pattern, easing to 2.8% from 3.3% the previous month. Monthly inflation also slowed: CPIH increased 0.8% in April compared with 1.2% a year earlier, while CPI rose 0.7%, again down from 1.2% in April 2025.

Core inflation also cooled. Core CPIH fell from 3.3% to 2.8%, and core CPI dropped from 3.1% to 2.5%, signalling that underlying price pressures—excluding volatile categories such as energy and food—are easing.

Energy Bills Deliver the Largest Downward Contribution

The most significant downward force on inflation came from housing and household services, particularly electricity and gas. The ONS notes that this category made the largest downward contribution to the change in both CPIH and CPI annual rates. This reflects the April 2026 Ofgem price cap adjustment, which reduced typical household energy bills and reversed some of the steep increases seen in previous years.

The easing of energy costs also helped pull down the services inflation rate, which fell from 4.3% to 3.4% for CPIH.

Motor Fuels: A Powerful Upward Shock

Counteracting the relief from energy bills was a large increase in motor fuel prices, which provided the most substantial upward contribution to inflation in April. The ONS highlights that this single category offset much of the downward pressure from energy and other transport components.

This surge in fuel costs reflects global oil market volatility and has immediate consequences for households, logistics, and business operating costs. It also marks a shift in the inflation landscape: transport, rather than food or energy, has become the most acute source of upward pressure.

Goods vs Services: A Mixed Landscape

The goods inflation rate for CPIH rose slightly—from 2.1% to 2.4%—while the services rate fell sharply from 4.3% to 3.4%. A similar pattern appears in CPI, where goods inflation increased from 2.1% to 2.4%, and services inflation dropped from 4.5% to 3.2%.

This divergence suggests that while supply chain related pressures on goods remain persistent, domestic service‑sector inflation—often linked to wages and local operating costs—is cooling more quickly.

The Broader Context: A Turning Point, but Not a Victory

April’s figures reinforce the sense that the UK is moving steadily toward more normal inflation levels. Falling energy bills and easing core inflation are encouraging signs, and the headline CPI rate is now within touching distance of the Bank of England’s 2% target.

Yet the picture is not uniformly positive. The spike in motor fuel prices demonstrates how quickly external shocks can re‑ignite inflationary pressure. Goods inflation is also edging upward, hinting at lingering supply‑chain constraints or currency effects.

The ONS data therefore paints a picture of progress, but not resolution. Inflation is cooling, but the path back to long‑term stability remains vulnerable to global energy markets and transport‑related costs.

The April 2026 CPI release offers cautious optimism. Energy bills are finally falling, core inflation is easing, and headline rates continue to drift downward. But the UK’s inflation story is still being shaped by volatile global forces—particularly fuel prices—which can quickly erode the gains made elsewhere.

For policymakers, businesses, and households, the message is clear: inflation is improving, but the recovery remains uneven and exposed to external risks.

The Outlook Remains Bleak

The Energy Price Cap Is Predicted to Rise in July

Multiple independent forecasters now expect a double‑digit increase in the UK energy price cap from 1 July 2026, reversing April’s temporary relief.

What the forecasts show

Cornwall Insight forecasts a rise to £1,850–£1,929 for a typical dual‑fuel household — an increase of £209 or around 13–18%.

EDF and E.ON Next forecasts sit in the same range (£1,847–£1,937).

Some models suggest the cap could reach £1,973 (around 20% higher) depending on wholesale volatility.

Why the cap is rising

The cause is not domestic policy, but the Iran war and the closure/disruption of the Strait of Hormuz, which handles around 20% of global oil and LNG shipments.

This has:

driven wholesale gas prices sharply higher,

damaged Gulf energy infrastructure,

and created a sustained spike during Ofgem’s assessment window (Feb–May).

Even if the conflict ended immediately, analysts warn that damage to infrastructure and supply chains means prices will not fall back to April levels by autumn.

Food Prices Are Likely to Rise Due to the Middle East War

Although April CPI showed easing food inflation, forward‑looking indicators point the other way.

Why food prices are under pressure

The Middle East conflict is creating a global “dual chokepoint” crisis:

Oil prices are rising, increasing transport and fertiliser costs.

Fertiliser shipments through the Strait of Hormuz are disrupted, reducing availability and raising global prices.

Shipping routes are unstable, increasing freight costs for food and agricultural inputs.

Crop yields may fall if fertiliser shortages persist.

Global evidence of rising food‑input costs

Fertiliser prices in some regions have surged 36–58% in a single month, nearly 90% higher than a year ago, directly linked to the Iran war and Hormuz disruption.

WFP modelling shows that if the conflict continues, global food prices will rise, pushing up to 45 million more people into acute hunger — a sign of severe global supply‑chain stress.

What this means for UK food prices

The UK imports:

fertiliser,

animal feed,

fresh produce,

and processed foods

from regions affected by higher fuel and shipping costs.

While the UK is not the worst‑hit region, global price rises feed directly into UK supermarket prices with a lag of 2–6 months.

Given the scale of disruption, food inflation is likely to re‑accelerate later in 2026, even if April’s CPI showed a temporary easing.

How These Factors Interact With CPI Going Forward

The April CPI report reflects past conditions, not the new shocks unfolding since late February.

What’s coming next

Energy bills rising in July will directly lift CPIH and CPI.

Fuel prices are already surging, and this was the biggest upward pressure in April CPI.

Food prices are likely to rise again, driven by fertiliser shortages, shipping disruption and higher oil prices.

Transport and logistics costs will feed through to almost every retail category.

April CPI is the calm before the next wave of inflationary pressure.

Read the ONS report 20 May 2026 HERE