Highland Councilís Debt Crunch: Rising Borrowing Costs Put 20?Year Capital Plans Under Pressure

6th May 2026

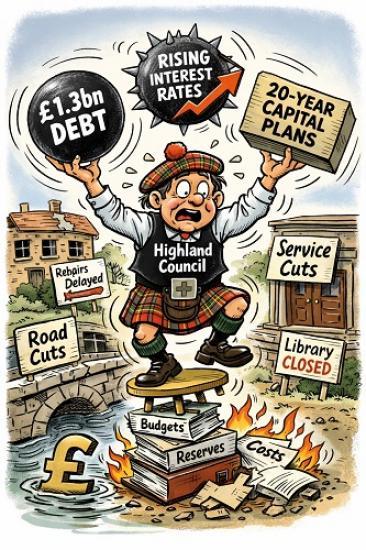

Highland Council is heading into a tougher financial climate than at any point since the financial crash and the pressure is coming from a direction that residents rarely see: the cost of government borrowing.

Following the UK’s latest rise in borrowing costs, the price councils pay for long‑term loans has increased again. For most Scottish councils this is unwelcome. For Highland one of the most indebted local authorities per head in the country it is potentially transformative.

This article sets out where Highland sits in Scotland’s debt league, why rising interest rates matter so much here, and what it means for the council’s ambitious 20‑year capital programme.

Highland Council: One of Scotland’s Highest‑Debt Authorities

Highland’s total debt now sits at around £1.3 billion, placing it among the largest borrowers in Scotland. But the more important measure is debt per head and on that metric Highland is near the top of the national table.

Debt per head (approx.)

West Dunbartonshire: £8,885

Aberdeen City: £6,666

Highland: £5,476

Glasgow and Edinburgh carry higher total debt, but far lower per‚Äëhead levels.

The Scottish average is £3,166 per person. Highland is therefore well above the national norm, reflecting the cost of maintaining infrastructure across a vast rural region.

This high starting point means that any rise in borrowing costs hits Highland harder and earlier than most other councils.

Why Highland’s Debt Is So High

Three structural factors drive Highland’s debt burden:

A vast geography with ageing assets

More roads, more bridges, more schools, more depots — spread across the largest local authority area in the UK. Maintaining and replacing these assets requires sustained borrowing.

Historic under‚Äëinvestment

Years of deferred maintenance have created a backlog in roads, buildings and essential infrastructure.

The Highland Investment Plan

A multi‚Äëbillion‚Äëpound programme to rebuild schools and modernise infrastructure, heavily reliant on long‚Äëterm loans.

Borrowing itself is not the problem — the cost of borrowing is.

Rising UK Borrowing Costs: Why They Matter

When UK gilt yields rise, the Public Works Loan Board (PWLB) — the main lender to councils — raises its rates. This means:

New loans cost more

Refinancing becomes more expensive

Debt servicing consumes a larger share of the revenue budget

Audit Scotland has already warned that Scottish councils face growing capital financing pressures. For Highland, the effect is magnified because:

A large existing debt stock means more exposure to rate rises

Limited reserves reduce flexibility

High rural delivery costs leave little room for manoeuvre

The council already faces a multi‚Äëyear funding gap

In short: rising interest rates tighten the financial vice.

What Is Prudential Borrowing — and Why Should Highland Residents Care?

Prudential borrowing is the system that allows councils to borrow for long‚Äëterm investment, provided they can prove the borrowing is affordable, prudent and sustainable.

It funds the big-ticket items:

school rebuilds

road upgrades

bridges and flood schemes

community facilities

major refurbishments

But prudential borrowing comes with a fixed cost: every loan must be repaid from future budgets. When interest rates rise, those repayments rise too.

For Highland residents, this matters because the council already carries one of the highest debt levels per head in Scotland. Rising rates mean:

more of the council’s budget goes to lenders

less is available for frontline services

capital projects become harder to deliver

council tax and charges may face upward pressure

Prudential borrowing is essential — but it is not painless.

What Rising Borrowing Costs Mean for Highland’s 20‑Year Capital Programme

Highland’s long‑term capital plan is ambitious, covering school replacements, road improvements, community facilities and major infrastructure upgrades. But rising borrowing costs change the affordability test.

Re‚Äëtesting affordability

The plan was modelled on lower interest rates. Updated assumptions may show that some projects are no longer affordable on the original timetable.

Re‚Äëphasing and delaying projects

To avoid taking on too much debt too quickly, the council may need to push some projects further into the 20‚Äëyear horizon.

Prioritising statutory and safety‚Äëcritical works

Bridges, school condition failures, flood defences and essential maintenance will move to the front of the queue.

Pressure on council tax and charges

If the council wants to keep the capital programme intact, it may need to raise more income locally.

Reduced financial resilience

High debt + rising rates + limited reserves = less ability to absorb shocks.

The risk is not that the 20‑year plan collapses — but that it slows, shrinks, or changes shape.

Should Highland Council Re‚ÄëExamine Its Plans?

Yes - it may have little choice.

A responsible council must re‚Äëtest its capital programme whenever borrowing costs shift significantly.

This does not mean abandoning the plan. It means:

updating interest‚Äërate assumptions

re‚Äëprofiling borrowing

prioritising essential works

being honest with communities about trade‚Äëoffs

Failing to do so risks locking the council into unaffordable commitments that would ultimately force deeper cuts to services.

What This Means for Caithness and the Wider Highlands

For residents and businesses, the implications are clear:

Some projects may slip

Budgets will tighten

Local taxes and charges may rise

Rural areas may feel the impact more sharply

But with transparent planning and realistic assumptions, Highland can still deliver a long‚Äëterm investment programme just not at the pace or scale originally imagined.

Related Businesses

Related Articles